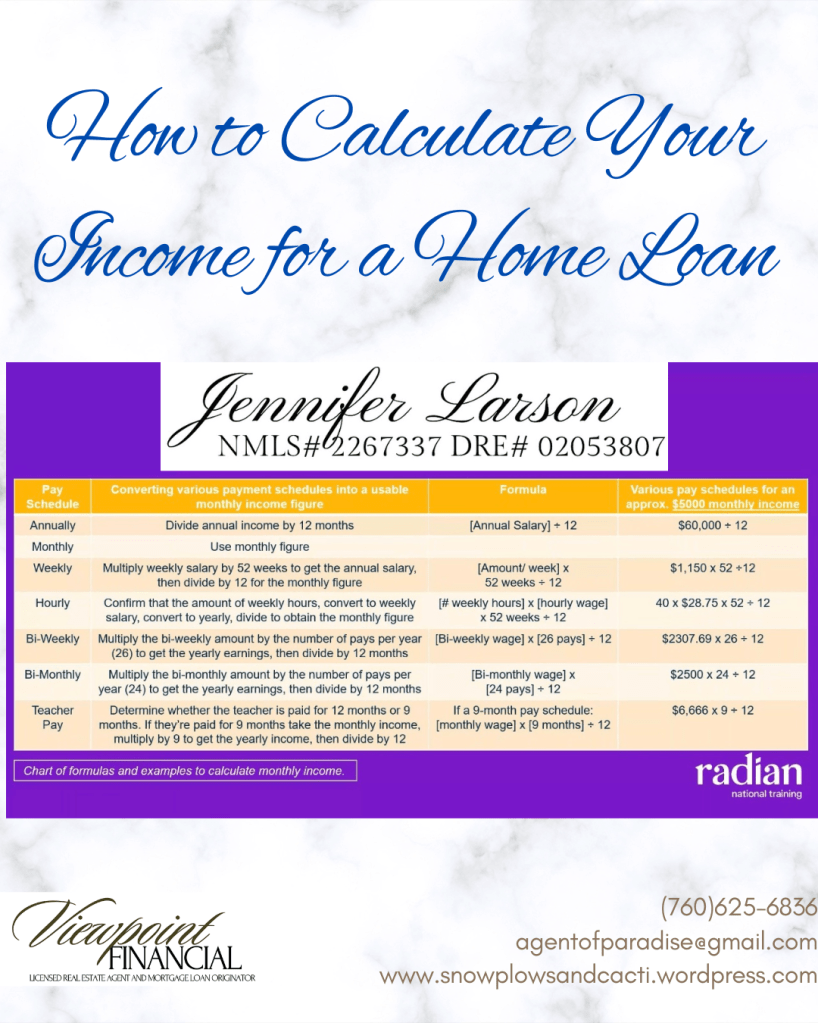

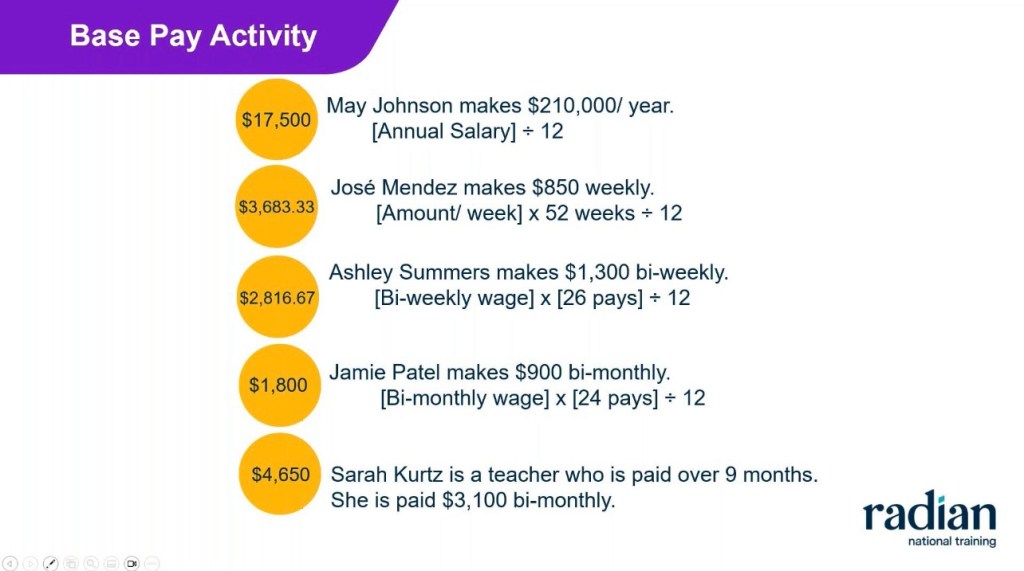

If you have seasonal income, most of your income comes from tips or commissions, or you have other income sources that might be inconsistent or part time, there are some things to consider when applying for a loan.

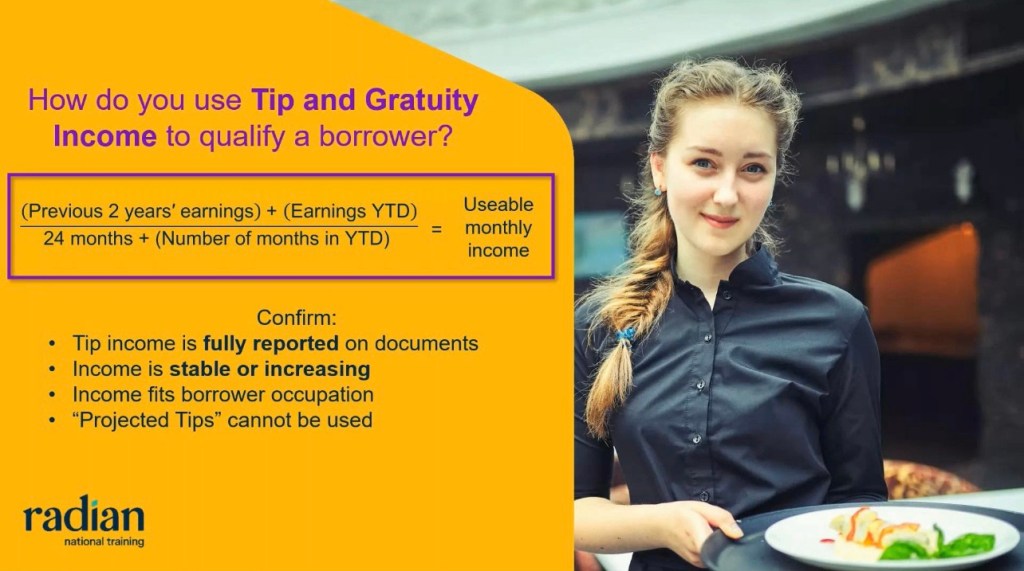

Some buyers make the majority of their income in tips like waiters, bartenders, other service industry professionals, etc. If most of your income is not in wages and you want to purchase a house with a loan, it is absolutely critical that income is properly documented as legal income. So many people love this method of income because they can make a lot of under the table money and avoid taxes. The problem is, as lenders and banks, we use your on paper income so if your taxes and employer tax forms don’t show how much you’re really making, we can’t use what you haven’t legally claimed as income. FHA and Conventional Loans require two years + of income verification and adequate documentation of tax returns, bank statements, W2s, etc.

Irregular monies do not help your loan application process in the way that we need regular and consistent money to use as income verification. If you occasionally get a bonus or the amounts are not predictable or consistent enough, then they are not likely to be included in your income; regardless of amount.

The main factors all buyers need to know is we need VERIFIED INCOME and we have a form for this, a VOE, and underwriting will investigate this with your employer and all financial statements to prove all documents are real and coincide with one another. That’s the biggest portion of escrow and why it takes so long these days. If your money isn’t well stated in forms and documents then it can take much longer for underwriting to verify and approve your loan if the transactions and numbers don’t make sense. Remember that the paper trail is what is most important for the banks issuing the funds to back your loan so make sure you are filing taxes honestly, annually, and stating all income. If you’re looking to save on taxes, the next posts will help you do that while still keeping your stated income high to get approved for a loan while paying less in taxes! Be sure to read the articles of March 2025 after this one to get the information or reach out for my Home Buyer Guide book.

I am a licensed real estate agent and lender in California but I can refer you anywhere in the country. Call/text (760)625-6836 agentofparadise@gmail.com for more information.