The last two weeks I have participated in the Fall One Room Challenge to makeover one room for two months. We’re working on our master bathroom and so far we have tiled and installed a new vanity, tiled almost completely the soaker tub surround, and for week 3 will be tiling the shower. The goal is to be completely done with tile by the end of the first month. Here’s where we’re at so far:

This is actually my second ORC of 2022. I did the Spring edition on my living room where I converted my living room closet into a built in coffee and wine bar with storage and style. For the Fall ORC, I decided to go bigger and do my entire master bath!

So here is where we started for Week One:

I mocked up a mood board of how we wanted to build out the master vanity area after we demoed and trashed the 1985 monstrosity which occupied the space before. It had a big giant typical mirror most original bathrooms had and everything was falling apart; even the medicine cabinet. So, we demoed completely and even removed soffits to revamp this space.

Here’s where we finished to begin Week Two today:

As you can see drywall is missing up top because we removed the soffit. We also refloated laminate floors underneath, put in the new vanity and plumbing, tiled the backsplash, and we are ready for the new week.

For week 2 we are removing the medicine cabinet, grouting the tile, installing small shelves, a second coat of primer, and hopefully mirrors! We also completely waterproofed the shower and laid out the tile to begin that this weekend. Stay tuned!

Should you still bother to move this year? Let’s talk about it. Obviously rates are going from low to high so now is the time to consider wants versus needs.

Could a move benefit you and/or your family? Will it improve your quality of life? Will it save you money or be worth the added cost? Is there a Life ROI attached to a potential move? Will you be happier?

If you answered NO to any of these, you need to thoughtfully consider if moving is a wise choice in your life right now. If it’s going to cost more without great benefit to outweigh that (Life ROI) then maybe now is not the time.

If you answered YES to all of these it’s probably smart for you to move. Analyze your finances, credit profile, and motivation to move and as a household make the decision to sell and move or purchase your first home. Talk to a lender to confirm your buying power and likely expenses.

Well, now it’s more complicated. There are conflicting reports about how rates will fluctuate but for the most part with rising inflation worldwide and here, the general consensus is rates may rise again this year as the fall progresses. In fact, they may not drop again until next year. No one knows for sure but the best plan of action is always to prepare to buy so when the time is right, your loan profile is ideal. This will give you the lowest rate possible and save you thousands.

In times like these it’s best to look at your finances and see what makes financial sense. If your mortgage is lower than current averages, can you afford that jump? Looking at inventory now, how much do you think you can afford? If what you are looking for is about $650k now, know the mortgage is over $4k if you only have an average 3-5% down; BUT, if you have tons of equity in your home you can subtract that amount and calculate the amount of sale price to determine how much you’d actually need to finance. So if you have $200k equity, can you readily afford a mortgage on $450k? If so, then yes, even with rates over 6%, it’s worth buying if you are able to get a home that better suits your family’s future. Prices are dropping a little again so you will automatically have equity in the new house and over the years you might have a total of what you paid in equity as appreciation goes up by the time you sell again.

In this market, buying and selling comes down to necessity. If you don’t need to move or really want to this year, then waiting is fine and you can see how the rates move the rest of the year. If they lower, reconsider again, and if they rise maybe wait until next year. Your home will hold most of its equity and eventually home prices will steadily increase again at the next rate drop; even if it’s small. Keep the property well maintained and updated reasonably and of course your finances and credit in good shape. When the time is right, you’ll be ready. If it’s not right, there is no benefit to rushing the decision and waiting is probably a sound choice.

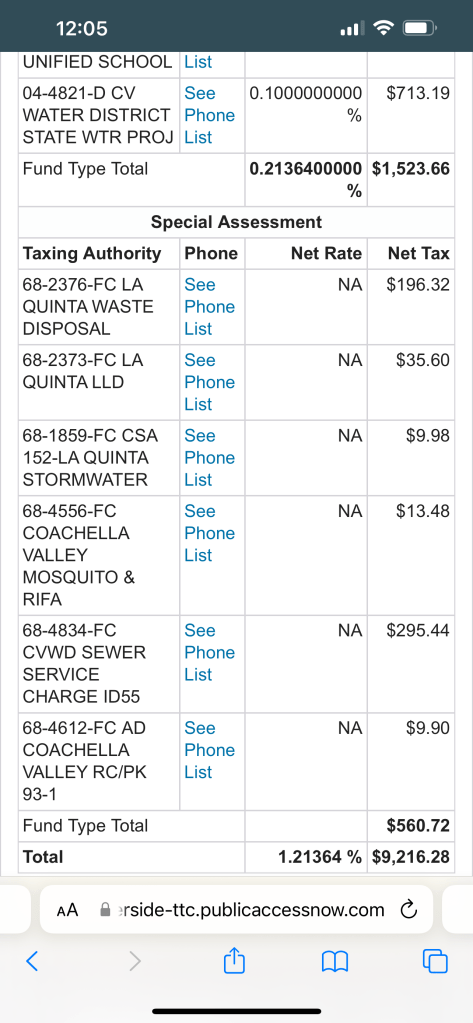

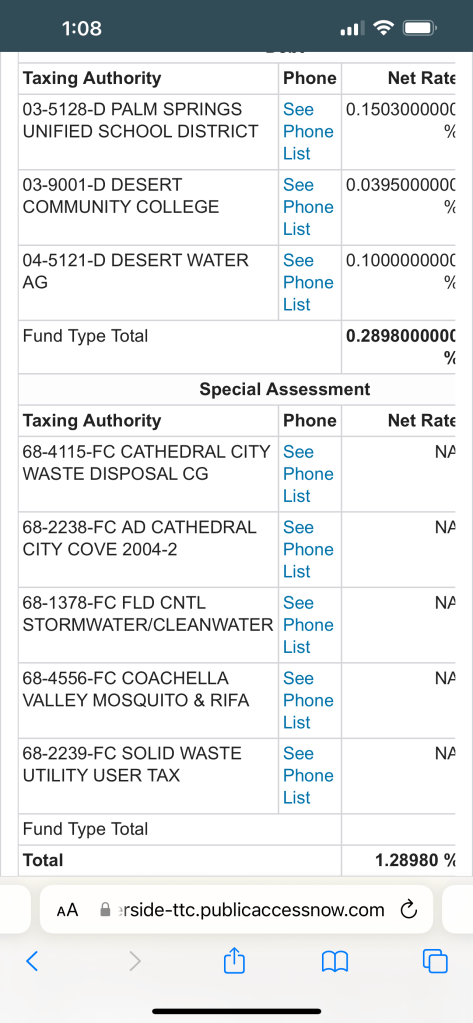

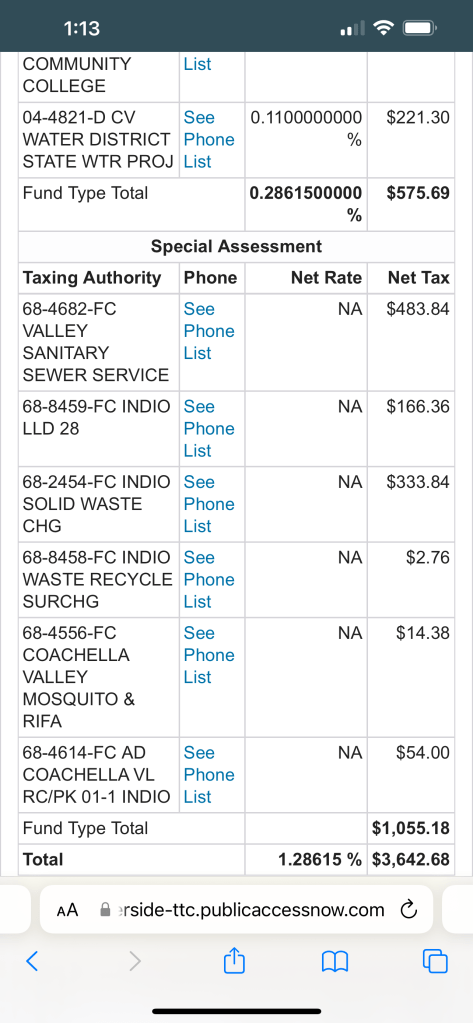

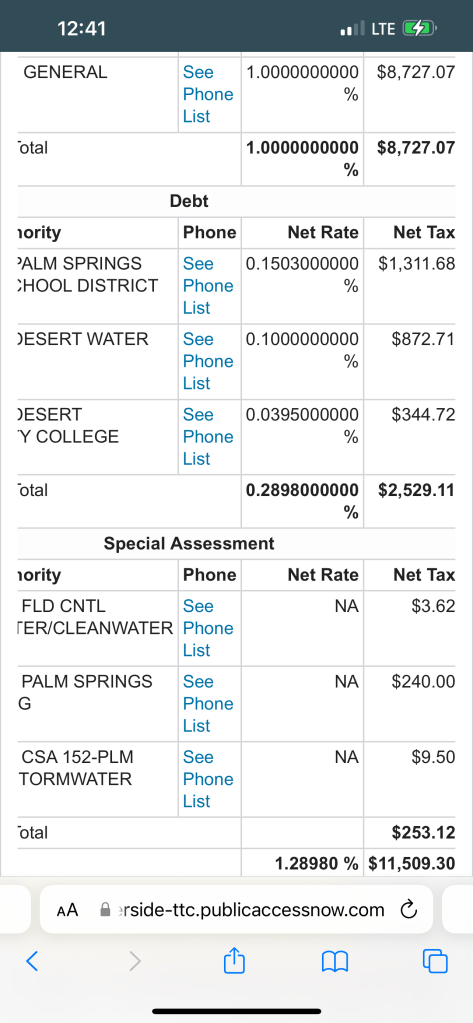

This is an overview of local property tax rates of popular cities in the CV.

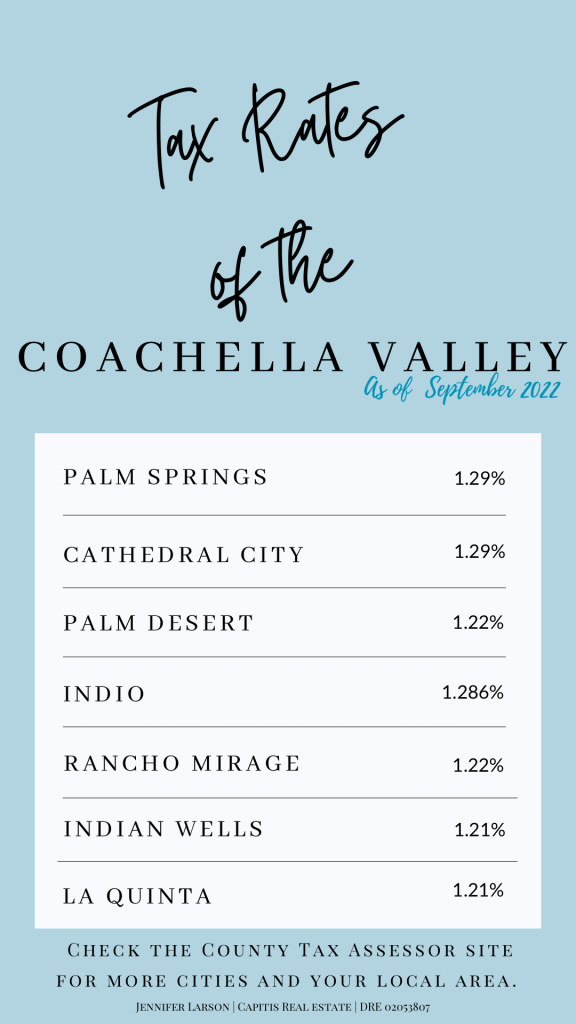

Here is a breakdown of the most popular cities in the Coachella Valley and their respective property tax rates.

As you can see La Quinta and Indian Wells are the lowest of the desert’s primary cities of residence of their 2021 bill.

Below I will share screenshots of actual homes from the area to show exact tax rates and their breakdowns of how they are allocated to city services. You will notice the city of Indian Wells not only has the smallest tax rate but also the shortest list of allocation because it doesn’t allocate to any vector control, sewer services, parks and recreation divisions, or even emergency services as individual recipients. The city uses its general fund primarily.

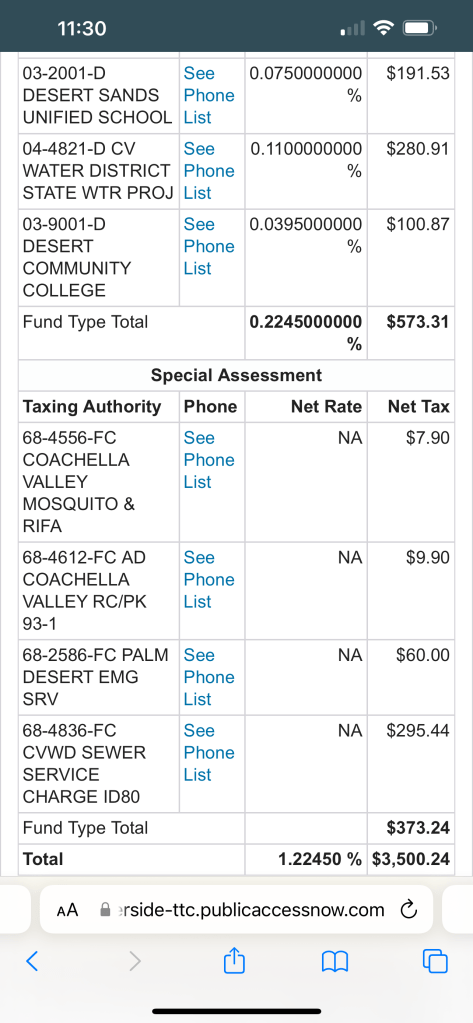

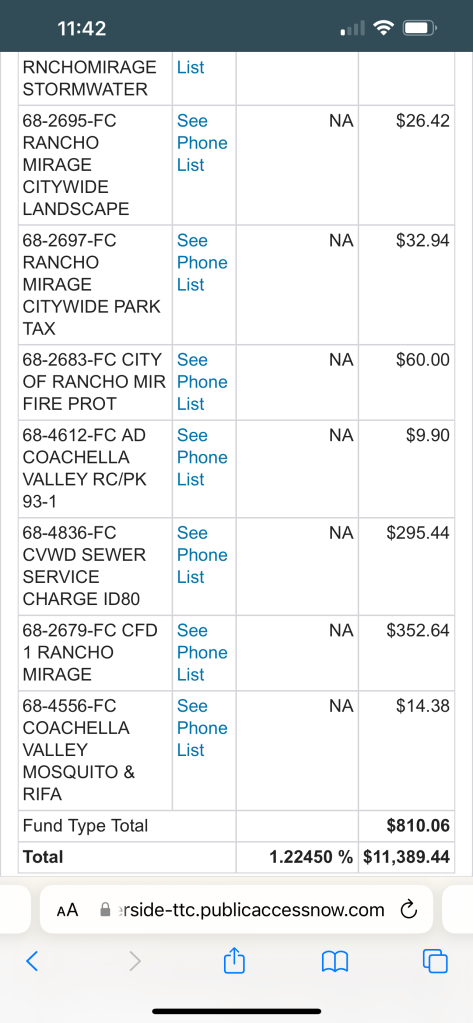

Actual screenshot of a property’s tax bill as of 9/14/2022 in Palm Desert.Actual property in Rancho Mirage for 2021 as of 9/14/2022.Full breakdown of a 2021 property tax bill for Indian Wells as of September 14, 2022. Notice it is significantly shorter and more basic than the rest of the valley.Actual tax bill of a property in La Quinta of the previous tax year as of September 14, 2022.Actual property tax bill of a recent sale in Cathedral City as of September 14, 2022. Actual property taxes of a home in Indio as of 9/14/2022.Actual property tax bill of a home currently listed on MLS in Palm Springs as of 9/14/2022.

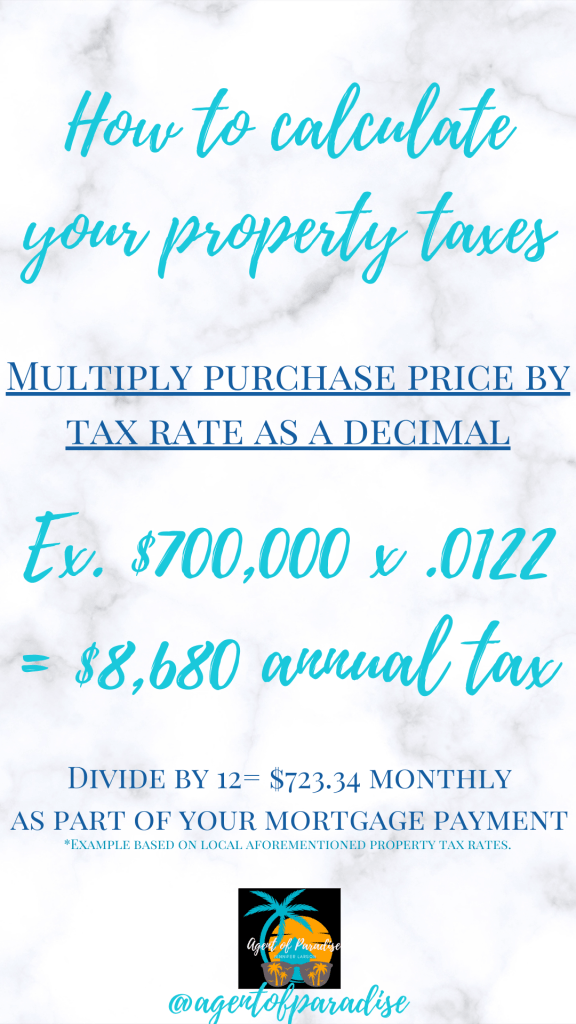

As you can see, property taxes throughout the valley vary and the rates will impact your mortgage payment as well as price at sale and slightly rise a little each year. So how do you calculate your annual and monthly taxes? Look below!

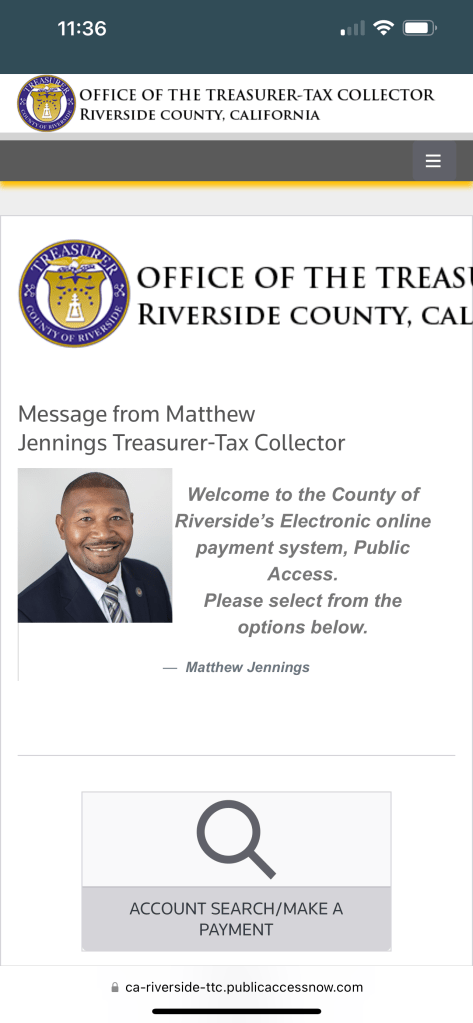

Remember that taxes go up maximum 2% every year, on average about 1%, based on the property’s last assessment (usually last price it sold at) until it is sold again and the new tax rate becomes based off the new sales price. Calculate your local tax rate off the purchase price of a home you are intending to buy. To look up local tax rates in your local area, visit the County Assessor’s site. For Riverside County here in SoCal:

Visit this website and insert the address you are researching.

Be careful with internet and Instagram advice from “influencers” and nonexperts.

I can’t say I believe in this because first of all, not everyone can actually afford this in the long run. I don’t know about you but I don’t have tens of thousands to short my family at the sale of my home! I NEED that equity and in the process of selling one home recently by focusing on every extra thousand we could get, it gave us the equity to purchase our next home in cash AND a new vehicle we desperately needed with a new baby. If I hadn’t, the rises in inflation and gas without the equity would have left me with no extra cash for either at all. That’s not a position I ever want to put my children in. Remember too, most people on Instagram talking about design and DIY are paid routinely by brands to keep doing rooms over in their home and design aesthetics so preaching that message is more about their wallet than yours. They’re in fact doing it for the money and so should you. Real estate is specifically about putting your money in a smart position to grow and purchase home after home with the same cash as you did your first!

Should you make a house a home to your desires? Of course! Just be careful about doing it cheaply, wrong, removing bedrooms and bathrooms that siphon up to $25k every time you do that from resale, worse in a down market, and make sure the work you do is quality that combines beauty and functionality. It can be uniquely you but also easy to convert to lots of equity when your family is in need of an upgrade for more square footage, perhaps a nursery for another baby on board, or to get some cash at sale for when you become empty nesters and need to send kids to college! Be smart with your money because ultimately that’s what a house is. Otherwise, rent is your best option and makes most financial sense.

Unless you do in fact have tens of thousands you don’t need anyway.

These are definitely not for everyone so talk to your lender thoroughly before committing.

I can get really technical here but it also gets confusing when discussing ARM loans to new buyers so I kept it simple with this quick video explaining how an Adjustable Rate Mortgage works in its simplest form how variable rates can significantly fluctuate your monthly payments.

ARMS are written like a ratio to represent the terms as a simple mathematical expression. For instance: a 3/1 ARM means the loan begins with an introduction of 3% interest on your mortgage payment. The 1 represents it will fluctuate every year to a specific index and margin rate in the future. We have no idea what the rates will be next year and every year afterwards. When shopping ARMs (if you don’t qualify for a conventional or FHA loan) is to lol for Hybrid ARMs with a low introductory rate (the first timber) AND a low lifetime cap rate (a third number) which is the max percentage rate you can be charged in the 15-30 years you finance for. This means regardless of how high rates go or how often the periods your loan terms adjust, your mortgage will not include rates beyond that lifetime cap. Understand that the rates gradually increase your payment possibly every year unless rates lower so you can be paying a higher mortgage every 12 months until that cal. If it’s a high cap you can be starting at 3% and rising over 8%! That’s a significant increase each month! More than double so BE CAREFUL with these loans; especially if you plan to live in the home more than a few years. Even if you don’t know, what if life throws you curveballs and you are still in the home a decade later with a mortgage getting out of control? If rates, your credit score, income, DTI, and equity are all in good order you can refinance to a fixed rate. If not, you have to sell or risk losing the home and everything you put into it. Those loans can be risky so BUYER BEWARE.

You may be able to refinance cheaper later but don’t count on it.

Could they all be right and rates will dip below 5% again? Possibly but the question is really when? Living in the hope it will be in the next couple years can be a foolish and devastating move if that’s your motivation for purchasing a home now. Maybe it doesn’t really matter if you are already dead set on buying; BUT, what if you are not because you’re on the fence about your finances, if this is really where you want to grow your career and family, or you’d rather wait until your credit and down payment savings are higher to offset the 6.5% you’re being offered (or 8% if it’s a no down payment assistance program)then it could in fact be best to wait until the follow year where it might actually be cheaper to purchase at a lower interest rate and market cost for you. In that case, the argument of a potential drop in rates may not be best because there’s an equal chance they won’t. If they do and you waited, you lose nothing because then you can buy at those lowered rates with the savings and credit you worked on for a few more months. However, if you let it persuade you before you were totally ready and the rates in fact DO NOT lower, you put yourself in a situation you were never comfortable entirely to begin with and if anything else in life happens, more inflation and gas prices, health issues, job cutbacks or whatever, you might be in a position where buying too soon is now causing financial burdens. That’s where this advice can hinder you. If you’re worried rates will rise and would rather buy and you are comfortable buying now then it makes sense. If the rates lower, great, refinance, and save money; BUT if you’re not ready 100% now and not even getting the rates in the 5s right now because of credit, DTI, down payment, etc sometimes waiting saves; especially if the inventory isn’t as good also. Some sellers are holding back and sometimes a year can change people’s tune waiting to see if a recession hit, prices go too low, they do need to move after all, etc.

So buy because it’s right in time and the home is right but don’t panic buy because you think you can get a lower rate next year. No one knows.

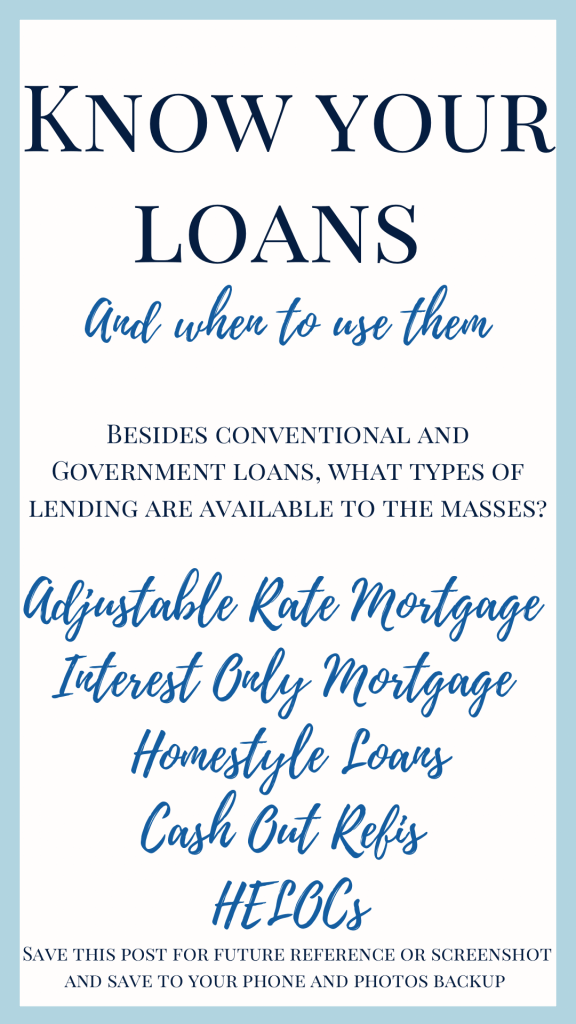

Most people are well aware of the common government loans such as FHA, VA, and USDA as well as conventional loans. Many people I work with don’t know there are an array of different loans that are qualified mortgages available to the masses by traditional lenders that are also sound options. How many of these have you heard of?

I will discuss ARMs in a coming soon post but here’s a basic overview of what they are and how they work:

Top facts to understand Basically their rates ebb and flow with the change in markets at the current time they’re impacting your loan, good or bad, how the economy is doing.

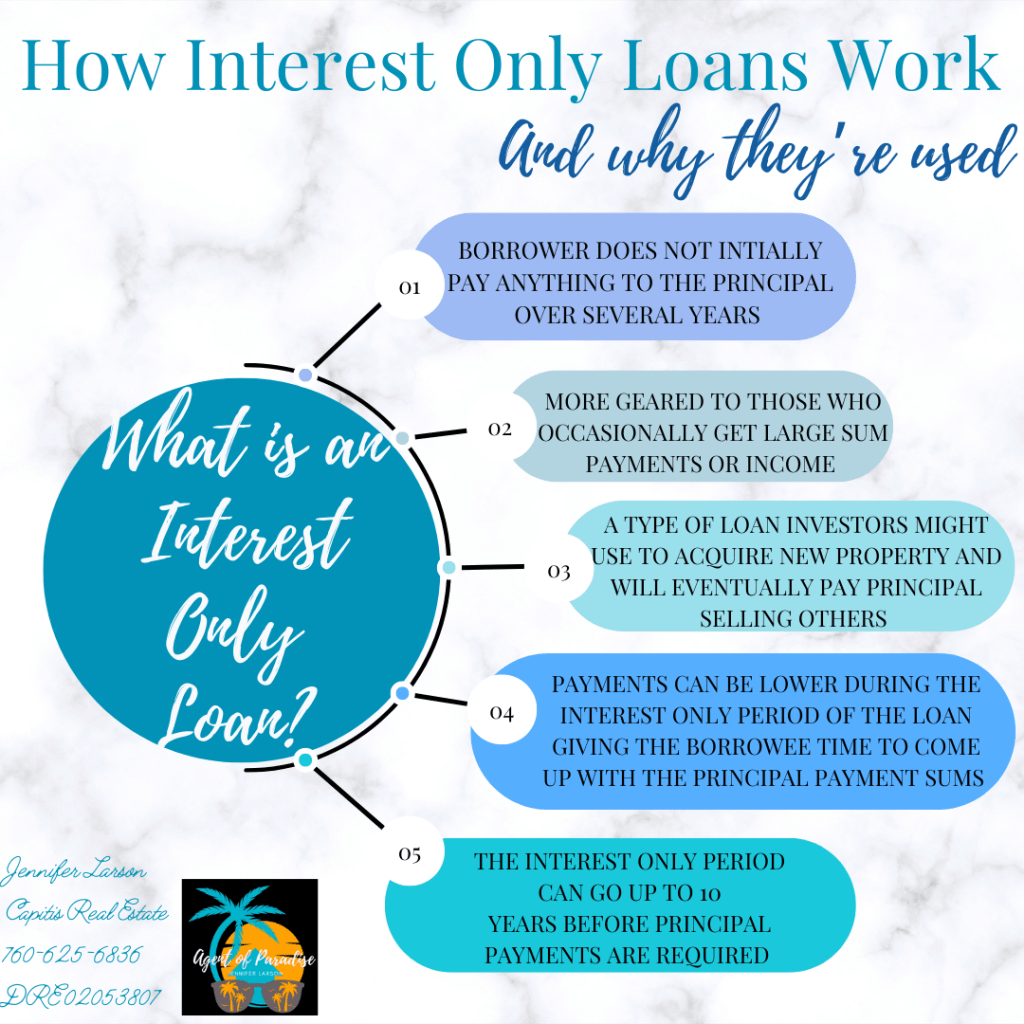

The next are Interest Only loans which are unlikely to be a best option for most but for a select few may be an ideal option such as military and those temporarily in their homes for only a couple of years.

These are critical to understand in their risks, reasons for use, and when not to use them. Talk with a lender and ask all the questions you have before deciding on such a loan product.

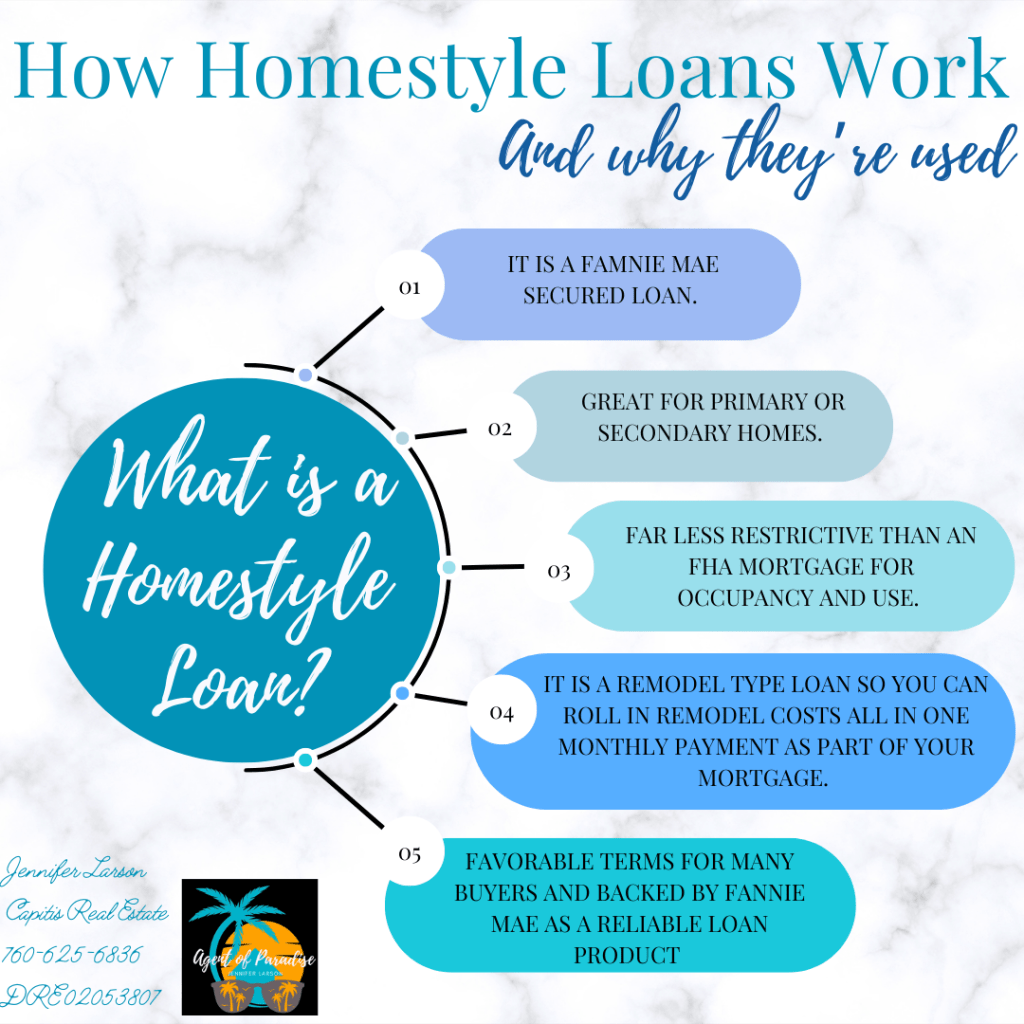

The HomeStyle Renovation Loan is one of my absolute favorites because of its versatility as a loan and tool for buyers with decent credit and DTI but not necessarily income yet. It allows buyers to purchase a fixer upper and get the costs of remodeling together in one payment in a stable loan program with oversight and streamlined financing of the projects. Here’s a breakdown how they work and what they are best for:

These loans have far more beneficial value to consumers but are relatively unknown in comparison to their FHA and construction loan counterparts. They do require review of plans, permits, financing, and inspections but so do reputable renovations in general and makes sure your GC is being honest with their invoicing and work timelines or they don’t get paid!

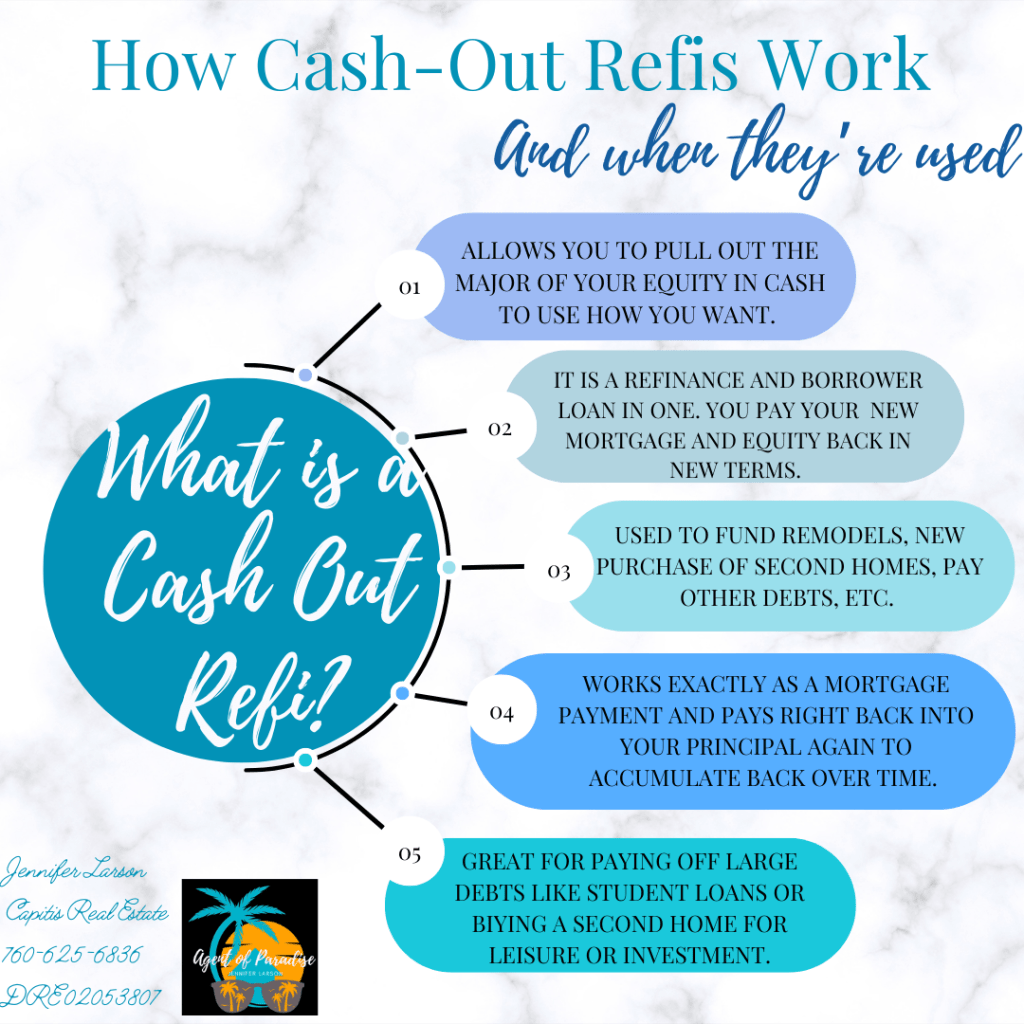

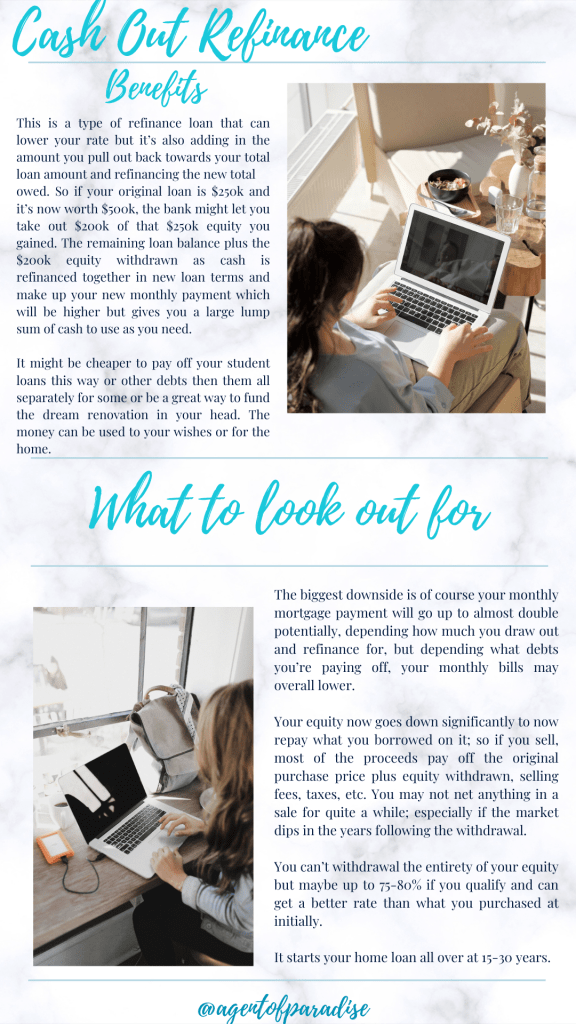

The next two are refinance and cash back equity options. The first is a Cash Out Refi, a refinance loan, that also allows you to take a majority of your home’s equity in a lump sum payment to use as you wish. Often people pay off debts, renovate the home entirely, use as emergency cash when they need substantial capital fast; or even for their dream wedding or vacation.

This works as a new loan on your home to replace the original and gives you your equity in a cash sum.You are basically rebuying your current home at its current market value and paying the mortgage now at that price so keep in mind payments are now going to be higher but possibly a better rate overall.

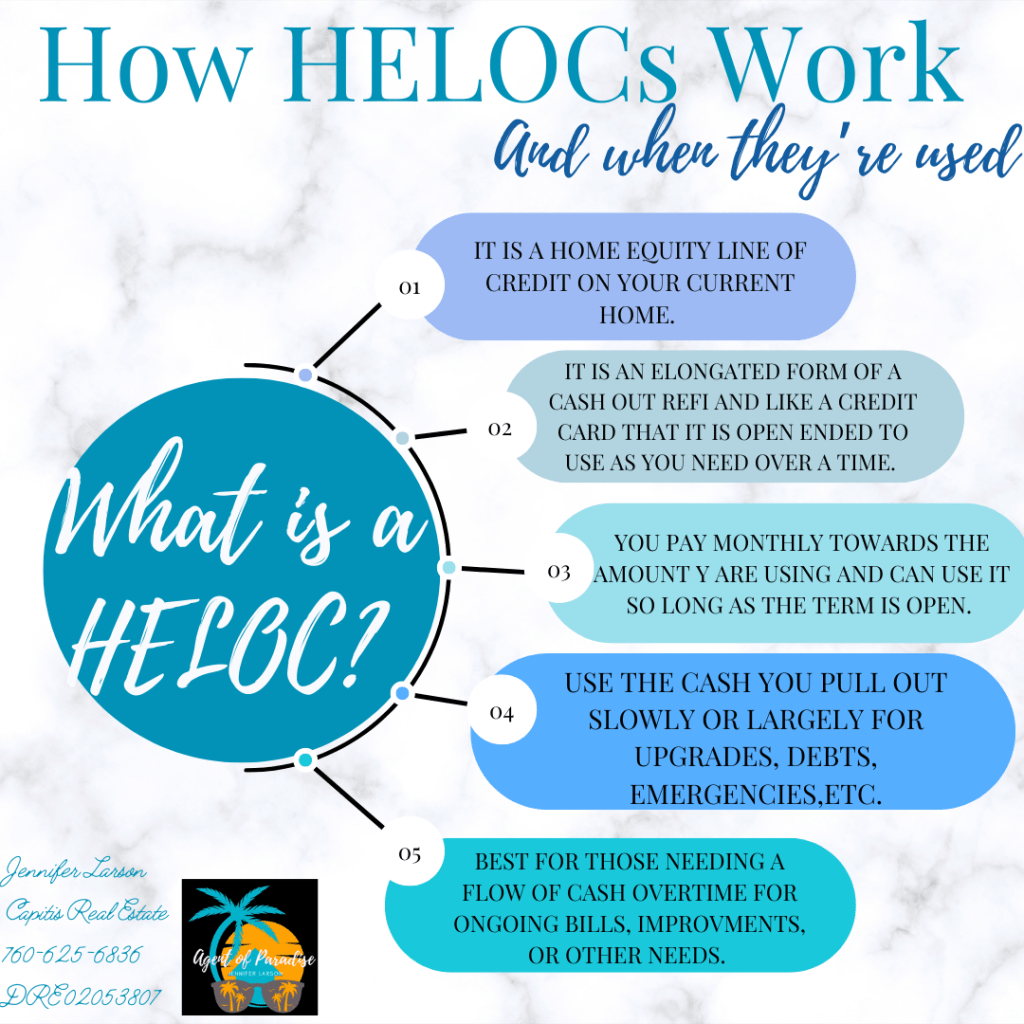

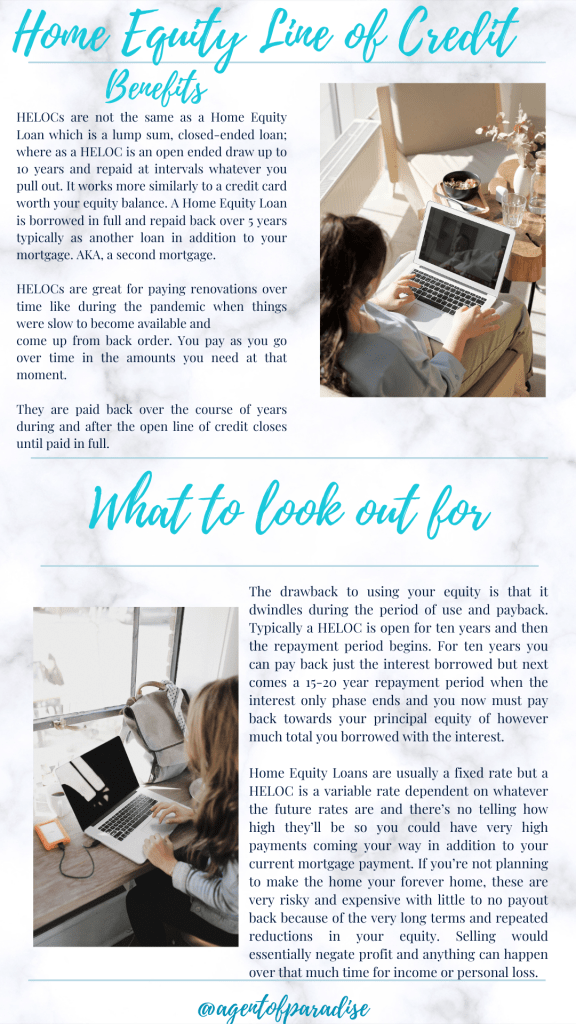

Lastly for today, we have the HELOC. A Home Equity Line of Credit, not to be confused with a Home Equity Loan, is an open line of credit on your home like a credit card that is valid for a decade as you need in increments and then closes to begin the repayment process.

Remember that Home Equity Loans are different and one sum payments. When people pull out a second mortgage on their home, this is one of the things they’re referring to. It does not refinance.

It’s easy to overspend and over assume the future of your income and stability with these so be careful and really talk over a HELOC with your lender about the long term. HELOCs are not a good option if you will be moving anytime soon or while your kids are still growing up.

That sums up today’s post on loans and Refi products. More coming tomorrow for renovations, new builds, more information on ARMs loans, and more! Stay tuned.

This is by far my favorite way to start putting more away to upgrade my home.

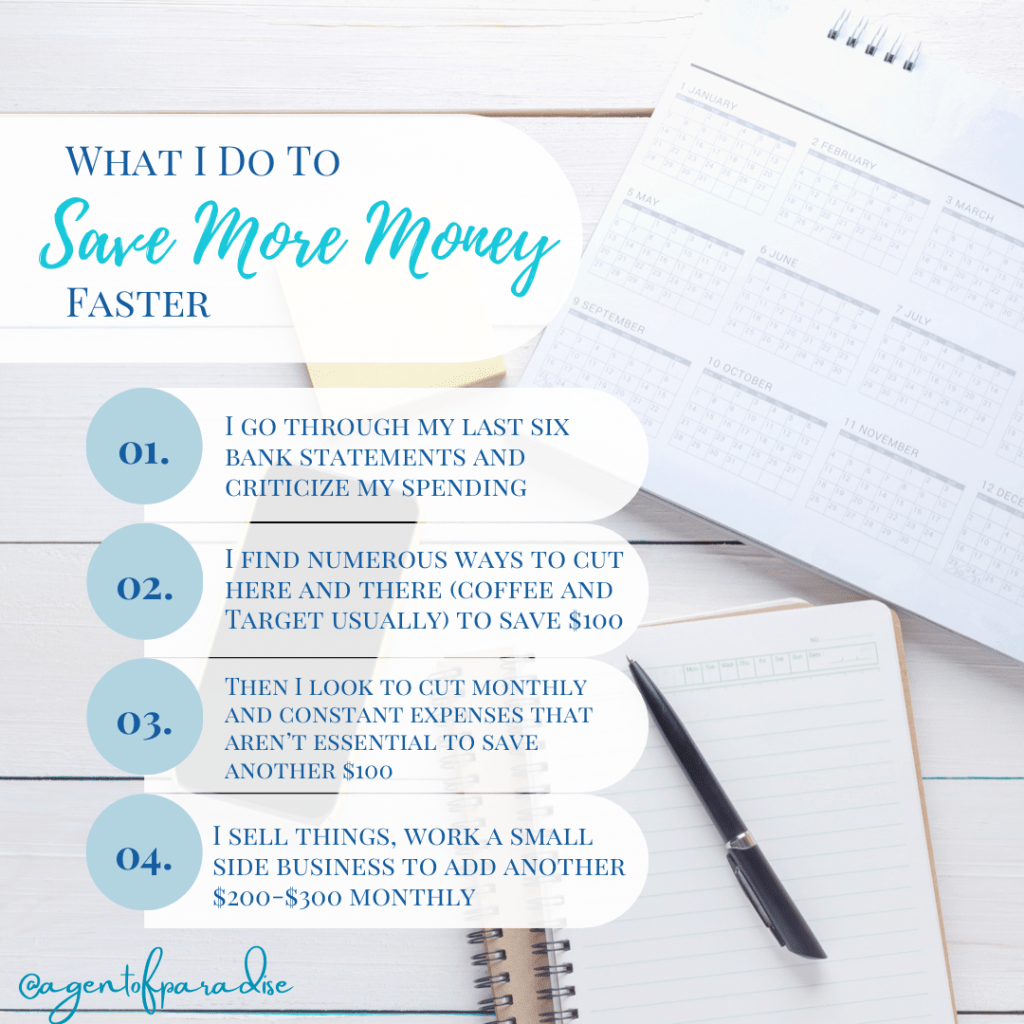

Saving money is HARD. It’s getting even more difficult these days to save money to buy a house and afford a down payment but it is possible. I have a few tips I recommend in this video and will outline further on my site. Here are the basics to get started: 🛠🪜

🏡 Analyze your bank statements and be honest with yourself. Be your biggest critic and decide if somewhere you could have saved an extra hundred dollars this month.

💵 Can you sell things, start a small business, pick up a part time job (which also helps you get a better loan rate and approval amount)?

💰 Cut nonessential services. I don’t personally have ANY streaming channels and haven’t for years. No Netflix, Apple TV, Discovery +, or anything. Nothing. I’ve got goals to tend to! 👩🏼💻

💵 Look at your spending and finances again. Can you save $150 each month between cutting streaming and going to Target and Starbucks less? How about $200?

If you’re not in a position to work a little more or save a few hundred dollars it’s probably not your time to buy; instead, focusing on building a savings account and follow a plan. Start with $100 or even $50 if you have to. Look at your grocery cart—is junk food costing you? How about fast food or eating out in general? How about alcohol?

Home buying requires healthy spending habits, goal stetting, saving, and more. If you’re not there yet, I can help you get there! It’s free so just ask. ☕️✅