Here’s a video of an actual conversation I had with clients, and many others, how they can be detrimental to your loan and approval amount. In the caption, I also explain some other things to consider. Including scenarios like this:

Lots of things to consider with HOAs. During your home sale you get a copy of the CC and Rs which is the rule book of the association so study them carefully and understand in depth. Ask any questions. You’ll also get the financial reportings of their dues and records of how the property is doing. That can impact your loan too if they’re not strong and also an indicator for you of incoming raises, additional bills coming, and maybe even deferred maintenance costs that can hurt your property. Thoroughly investigate the property yourself and look at all the units and amenities as a whole. How do the pools and clubhouses look? How are the sidewalks and roads maintained? Are the gates and steps safe? Do you see roof and exterior issues because those are managed by the HOA and their responsibility as part of your dues paid.

Be vigilant and diligent. Read the disclosures too and talk to neighbors. Meeting notes from board meetings and member comments can be very useful and you’re entitled to those as well before closing.

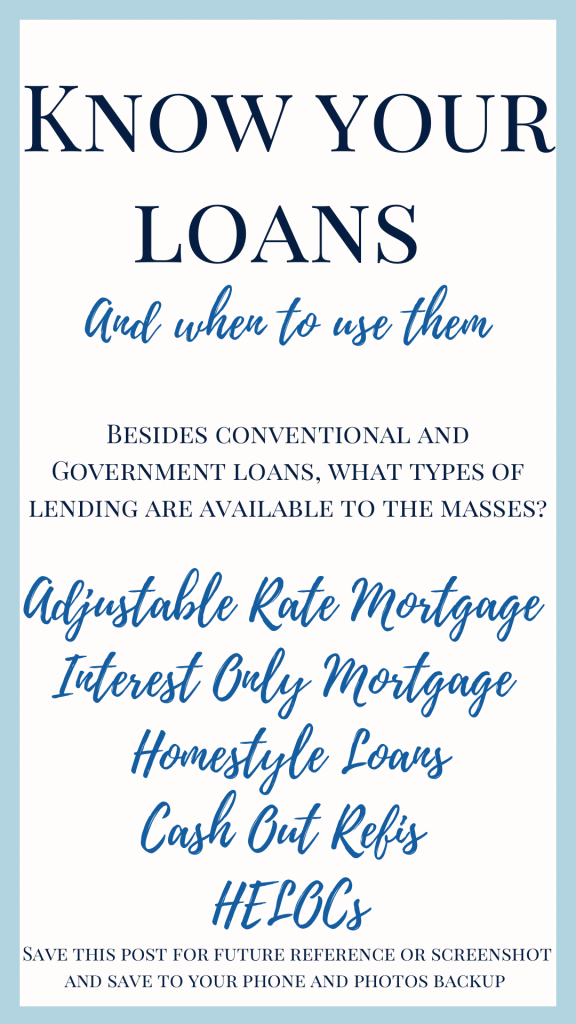

I’ll post a few information graphics below to share for you to research before applying.These are my last resort almost but good to know.

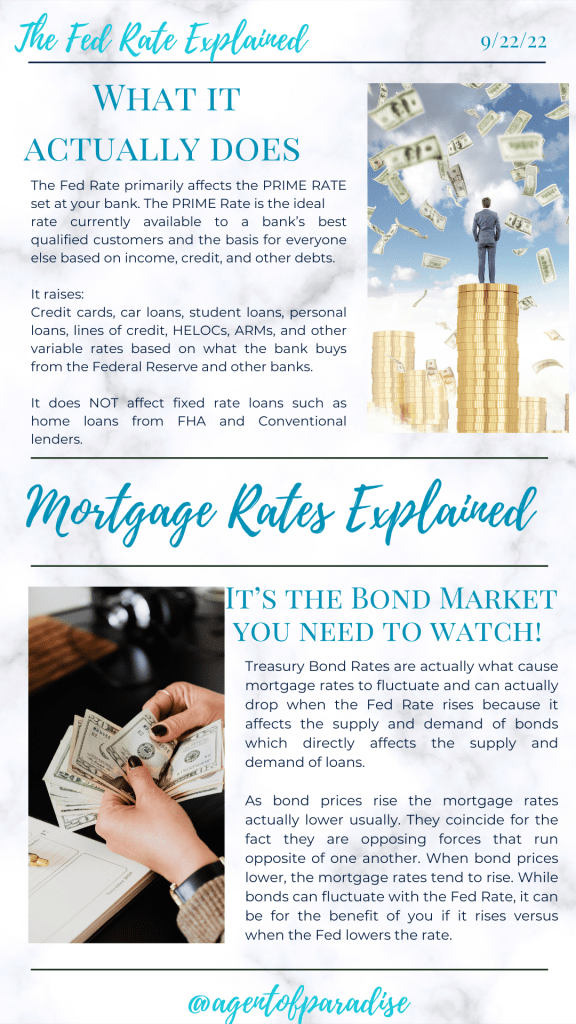

ARMs can get very expensive and these loans often are based on the PRIME Index (the Fed Rate) but even when the Fed lowers the rate a lot, you’re still paying a margin over the Fed Rate. The Prime Rate could be 4% but your ARM could still mean you’re paying 6-7% because of your margin on your loan. The Fed Rate is the base of the loan but rarely what you actually pay. You can get low rates in the beginning of ARMs and refinance as mortgage rates drop, if you qualify and have the money, but otherwise you’re stuck in them and they can rise to 10% easily at a lifetime cap. Be careful on these.

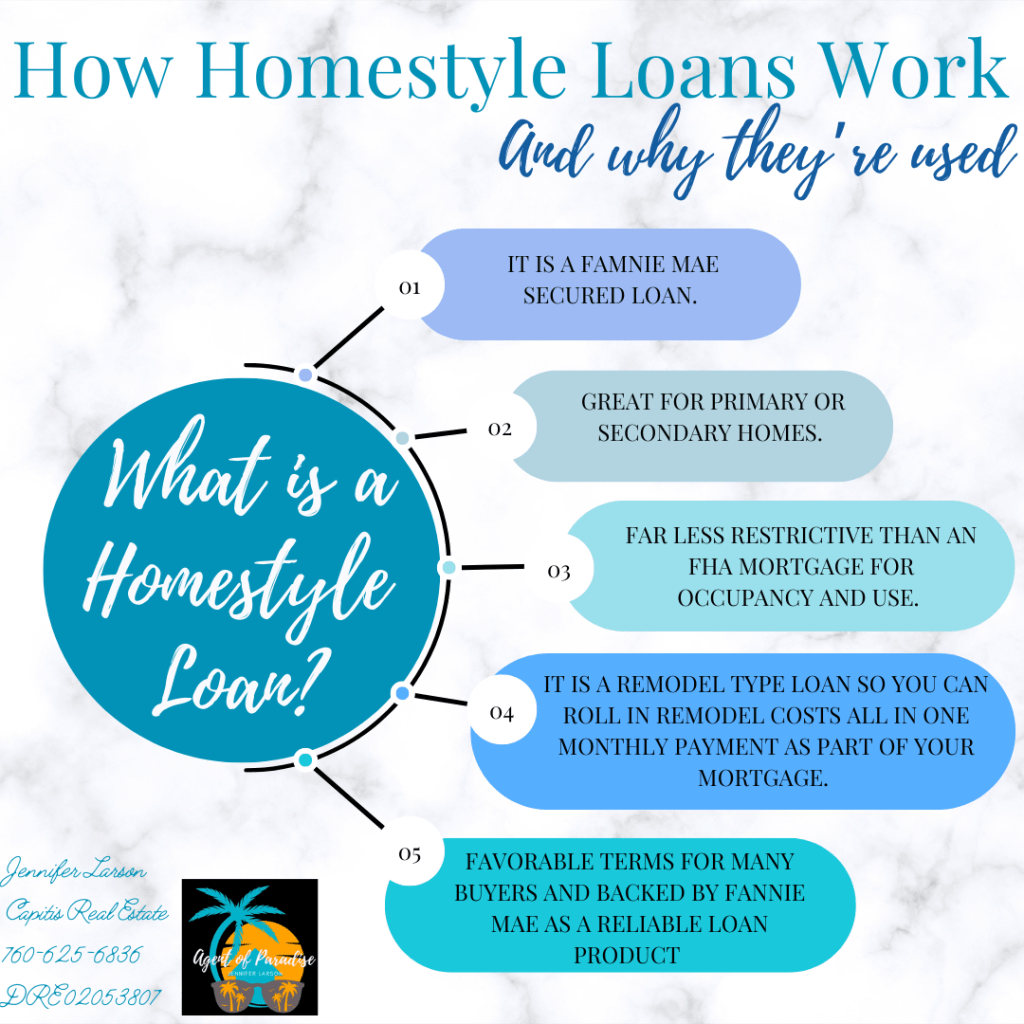

This is a VERY long term plan and best for experienced investors.These are one of the few FHA loans I prefer.

HomeStyle Loans are great because even though they are FHA they don’t have the rules and regulations of FHA. From day one you can use them for STR, flips, LTR, etc and they roll in the construction costs and they actually force the GC to be accountable. These loans require a 6 month turnaround, only approved contractors and engineers, they disperse the funds based on work completed, and they do lots of inspections. I like these for the average person even if they don’t want to invest. They’re fantastic and in less expensive markets, they’re going to cover a lot and help you find a home you actually want to live in, that might currently be scary to consider.

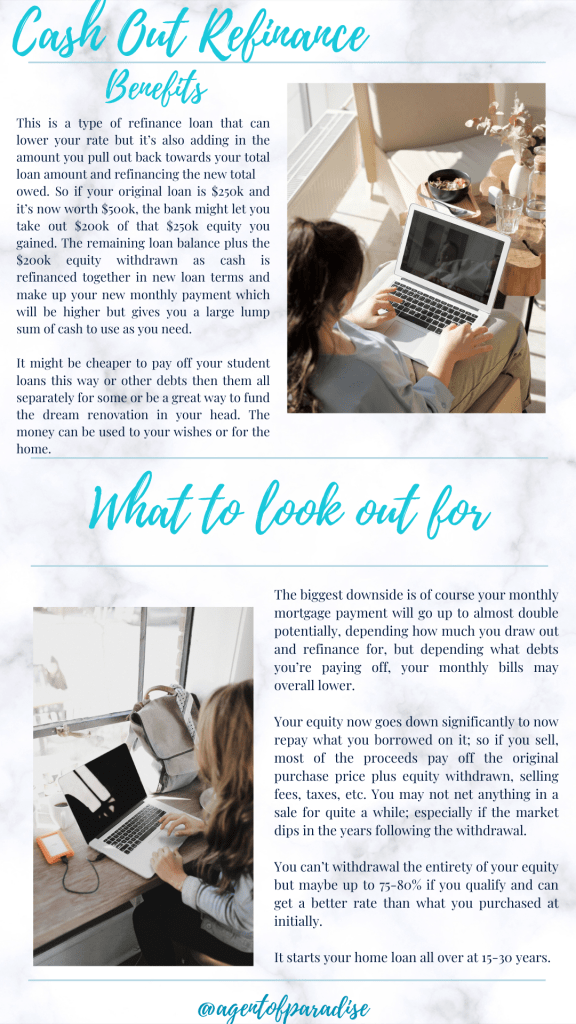

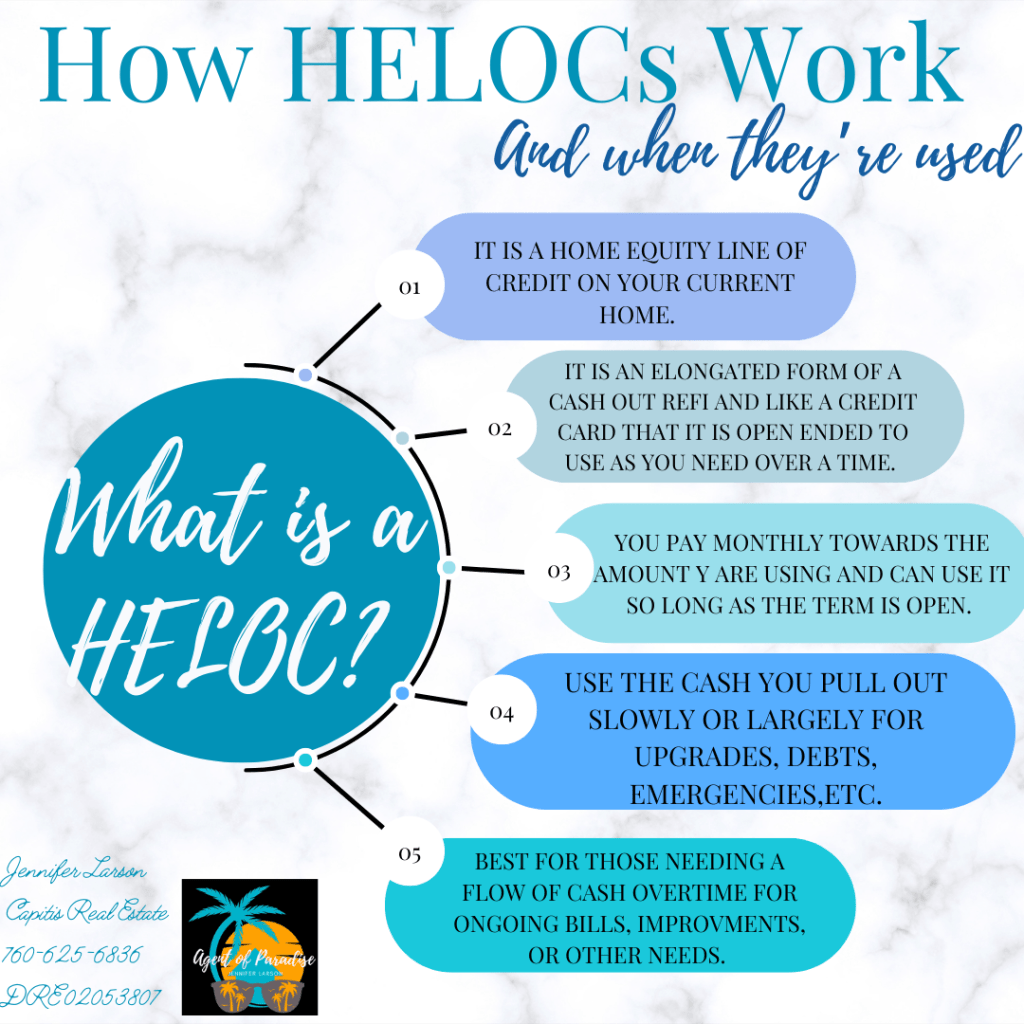

These are when you want cash but not to move.Understand these are a second mortgage against your house.

These can be great if used right and you’re smart with how you plan because it’s a loan against your home’s equity so understand you have to pay it back with your mortgage. Basically you refinance your house at its current value which is a lot higher and you after fees and taxes you get about 75% of your equity in cash to do as you please. This is where you need to be smart. Since you now have a bigger house payment don’t go buy more things. This should be used to pay off student loans, pay down all other debts, buy an investment property or pay one off, or you can use it to out kids through college etc, but be smart. It’s not free money and it can wreck you quick if you don’t get smart with it.

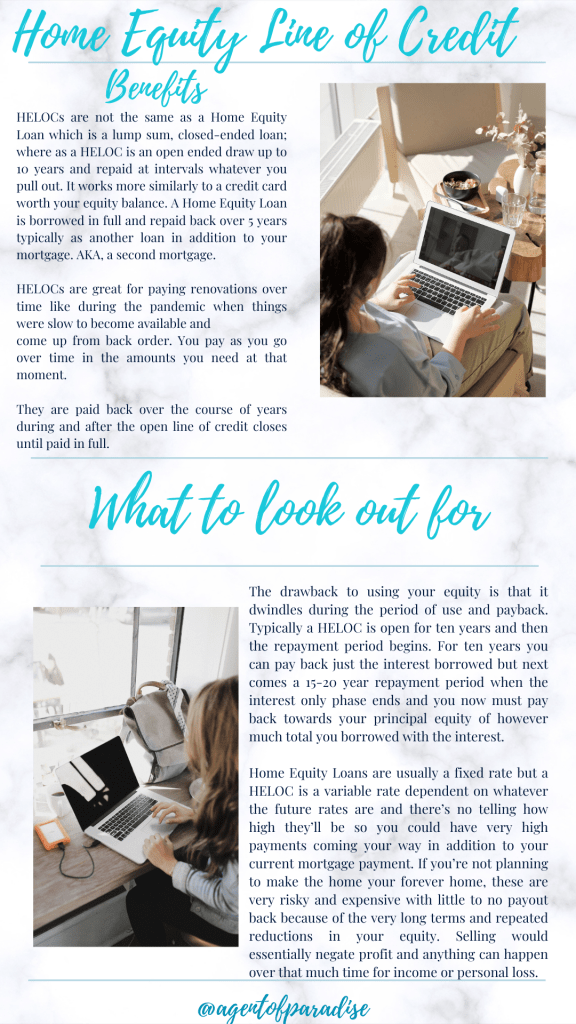

This is like an ongoing credit card against your house that expires.This is a line of credit you can use as much as you want as long as you keep paying down and it’s usually good for ten years. You can use it multiple times as long as you’re paying it down.

This is basically using your home’s equity as a credit card 💳. You can charge it up as much as you want and as long as you pay on it, for a decade you have this extra cash to use. However, like a credit can get you in trouble imagine how much trouble and debt you can incur with a six figure credit card limit if you’re being stupid with it. Again, this is best for life expenses like paying off all your other debts, student loans, renovations that put the equity back in, some do use it for weddings, paying off medical bills, using it to travel, etc. Have a PLAN with this and remember it’s a big credit card bill every month if you’re not using it wisely.

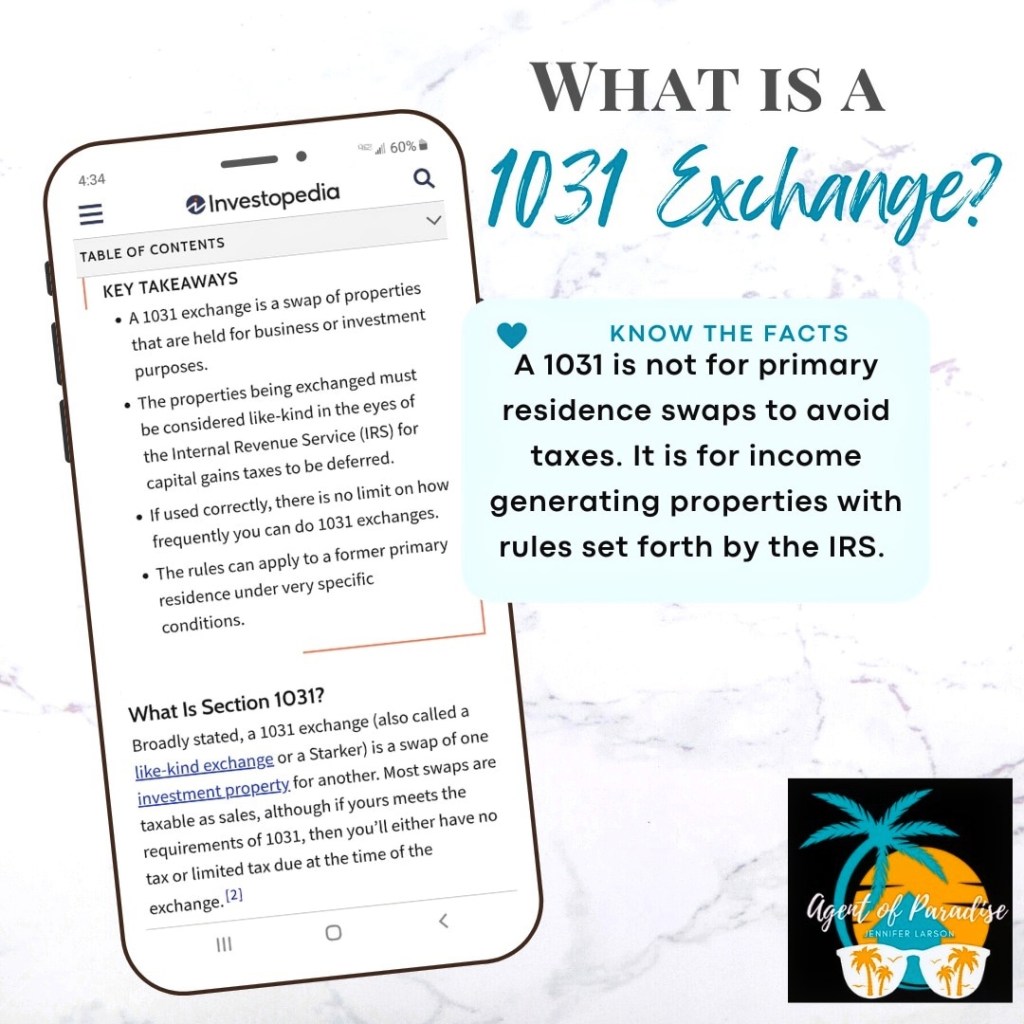

This is another option and you need a 1031 expert to facilitate the sale.

I have done these with clients and they work the same for us as agents on a 180 day deadline which is more than enough so long as you know what you’re buying, and get into contract relatively quickly. Escrows do get extended, canceled at the literal closing (been there) and other things can fall out and you have to start over again, maybe even with your home search and loan. I’ve had escrows that were supposed to close in two weeks suddenly take 4 months, multiple times. This kind of home purchase requires you to be smart with your time or you mess up your finances. You also need a 1031 Exchange agent because this is what’s called a Tax Deferred Sale and there is a lot of backend paperwork involved. It is a good option though!

Of course there are way more programs but these are the ones many people know but misunderstand the most in my experience. A good lender will show you all the options!!

Most people have this problem because money is hard to come by obviously. The answer to this age old question is throughout my blog and Instagram actually because it’s multi-faceted. You need the right savings and checking accounts like the MMA and HYSA and definitely a CD or two to keep that savings out of reach for spending but still earning great profits on your money. Those are all tools to grow your money.

To get more money I constantly share savings plans like $5 HYSA contributions or $100 per month, or swapping your streaming and television services for deposits into your account because that’s how money grows fast and gives your more time in life for the things that matter. I share a more efficient plan for those who can afford up to $250 per month and I share how to get to that and make the right cuts and changes to minimize the impact on your life but also maximize the impacts on your financial future.

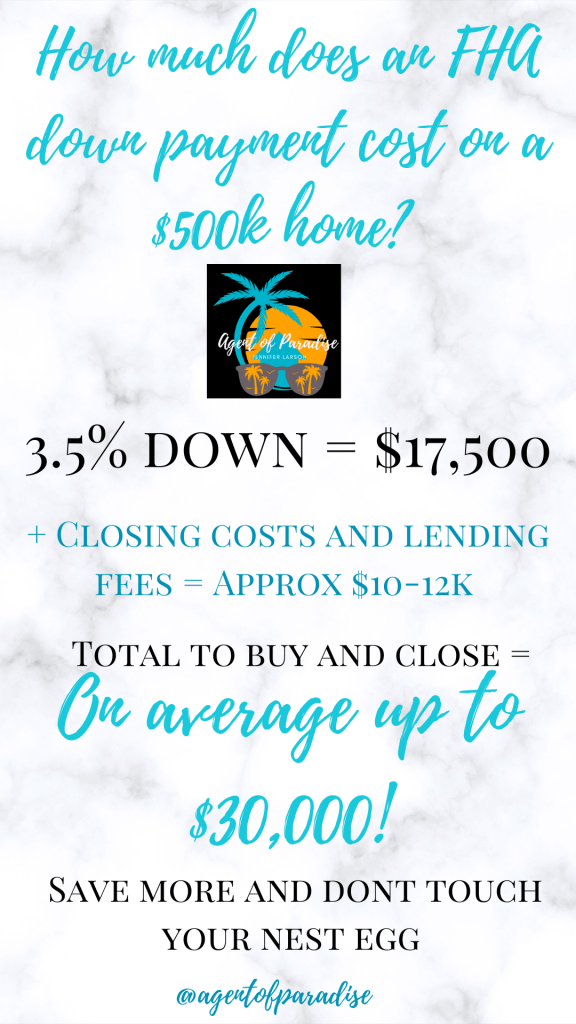

How much do you need? Well, here’s a starting point to consider:

There’s a conventional first time buyer program that’s affordable at 3% down and no upfront MIP if you have good credit and income and haven’t been a homeowner for at least three years.

If you need a personalized savings plan, send a DM to @snowplowsanscacti and I can help you there.

If you need help, just DM me at @snowplowsandcacti on IG.

This is a good starting point if you’re thinking about buying a home one day. You have to be consistent with this. You don’t need to be debt free to get approved for a good rate usually, but you need a low debt load in order to get the best rate and lowest monthly payment possible.

Car loans are absolutely a killer to your approval chances, rates, and approval amount. The more debt you have, the more risk to the lender, so the more they’ll charge you to cover that risk. A lender is like an interviewer you want to look good and present yourself as best as you possibly can so make sure you have your finances in order and your credit cards aren’t charged high. Keep your balances, and usage low. It’s how much you CHARGE every month that matters and affects your score. Keep that in mind and don’t finance anything else in a monthly payment plan because that’s bad news for your loan application. Keep debt low and then you’ll have more to make your savings higher.

The more I look at rates, prices, the current affordability aspect of America, I do believe it’s time to revisit the aspect of doing a minimum 5%. You can do any amount technically that you want to put down, it’s just some programs have a minimum. If you have 7% down for what you’re seeing on Zillow, you can absolutely do that, and should if you’re financially ready. You can put any percentage down too if you decide it’s financially best for you to wait a few years and but say 12-15% down. What works best for your finances is when it’s best to buy. Yes, there are better markets than others and “buying the dip” certainly works well in real estate but it also needs to be when your finances are in a good place. Those factors need to coincide for it to be the right time to buy for you.

I know I sound like a broke record but I’m a huge believer in getting a high yield savings account and just putting money away. You don’t need a reason to save except to save. One day, your car is going to die. You might have an expensive medical issue in your family that’s going to pile on debt. You might want to have another child or begin a family. Maybe one day you’d like to go back to school if you can afford it and the kids are a little older. Maybe you’d like to buy a car in cash, even used, but you have no money. Even if you need tires one day, aren’t they so expensive and hard to afford because they go out at the worst times? Doesn’t it rent, then pour when you need sunshine the most? That’s why you need reserves.

So how do you build reserves on a very tight income? I always tell my clients to start with $25 per week or $50 per paycheck if you’re paid bi-weekly (every two weeks). Many people say they can’t even afford that, but, I know from experience, to do it. I have been there too. I spent many years not being able to afford the electricity and getting service shut off multiple times, only being able to pay part of the bill so I did to at least keep it on when I could. I was so sick of being broke and realized I needed to make a change. I figured if I’m already struggling to pay or can’t pay, I might as well struggle a tiny bit more but because I am putting money away. I walked or took the bus when I could to save on gas, or carpooling with coworkers. I got more frugal with not turning lights on, unplugging anything not in absolute need to be plugged in, stopped even turning the TV on, and opened the windows for a breeze instead of turning the fans on and learned to live with my AC not as cold as I wished. I saved A LOT or what was a lot to me at the time. I stopped with Netflix even way back then, lowered my interent plan, and cut the cable. All of those savings I added up. I think it was around $237 which was lifechanging at the same because I barely had $2.37 to my name, let alone without the decimal. I decided to put $200 of my paycheck contributions into my 401k in addition to the already $50 they autoenrolled per paycheck. They were matching our contributions at the time so I was getting the full amount. Years later when I left, I had a down payment for a house because I totally forgot about that account!! So did my husband. We built wealth from there with our condos, then houses. But to get started, it was those small amounts per paycheck changing everything and we didn’t even realize. It wasn’t a sacrifice it was the only reason we weren’t broke today.

Nowadays I know about tax implications of pulling out your 401k and filing that on your returns so now I know to just open an HYSA and put that money in. Don’t touch it! Let it rise like sourdough bread and see how it changes your life. Are on the same trajectory to be broke 5 years from now? Then get an HYSA and put money in it. You in 5 years will be a lot happier. Even if you don’t want to buy a house then or decide to wait another few years, you have a nest egg just to keep growing. One day you’ll have it for an emergency, a bigger downpayment so your mortgage will be smaller and easy to handle, or you won’t have to work until you’re 80. If you are hoping to buy a house one day, I would shoot for at least 5% down and remember that a starter home still works like a badass bank account to make you money in another 5 or so years, even better than an HYSA, and no asshole landlords to deal with! Don’t focus on buying your dream home but an improvement over what you have that you own and will grow your networth so when you sell, you get what you paid, and then a whole lot more. It’s better than renting for that reason alone but ONLY if it doesn’t stretch you too thin.

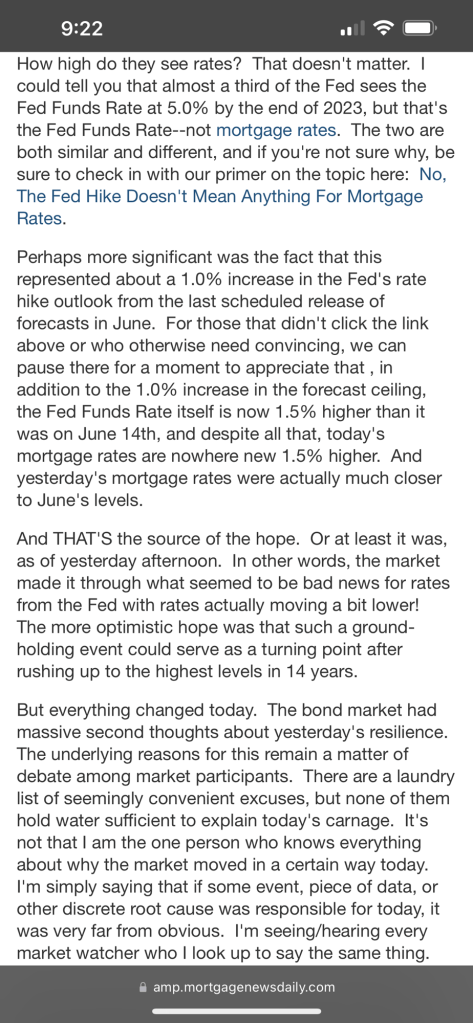

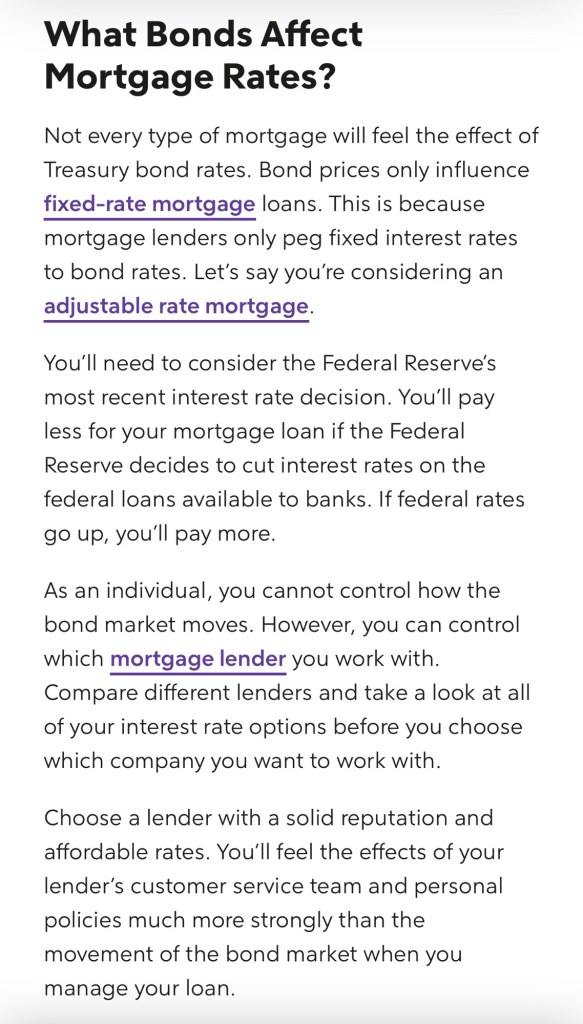

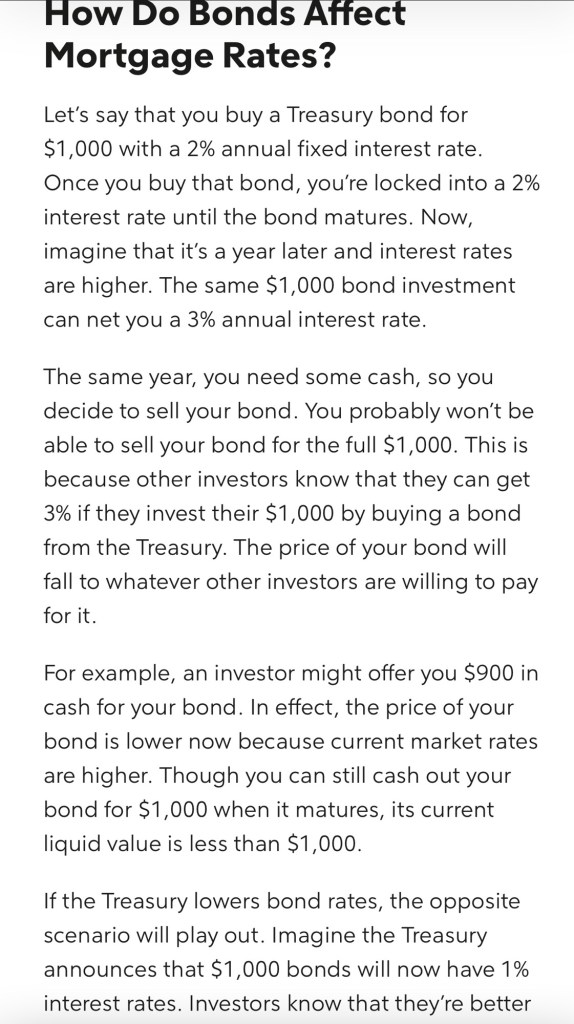

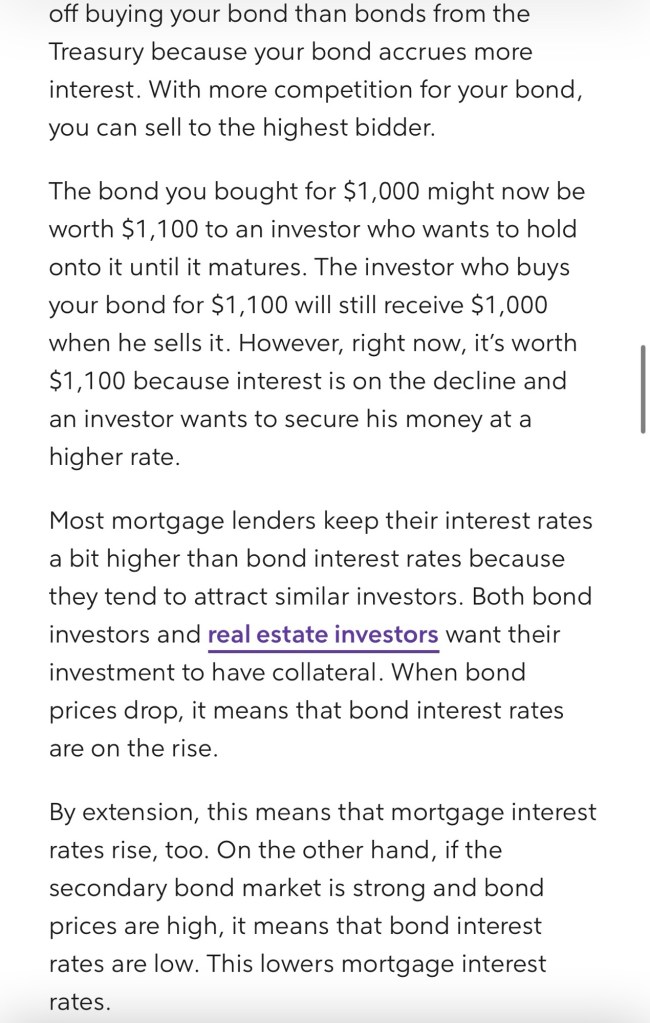

I also have a longer explanation at http://www.womenbelonginthekitchen.wordpress.comThe two rates can coincide but they’re not the same and the Fed Rate can change nothing sometimes for mortgage rates.A quick example why they can sometimes affect each other.From Rocket Mortgage Part 2 belowHope this helps!!

If you have more questions email me or send a DM @snowplowsandcacti on IG.

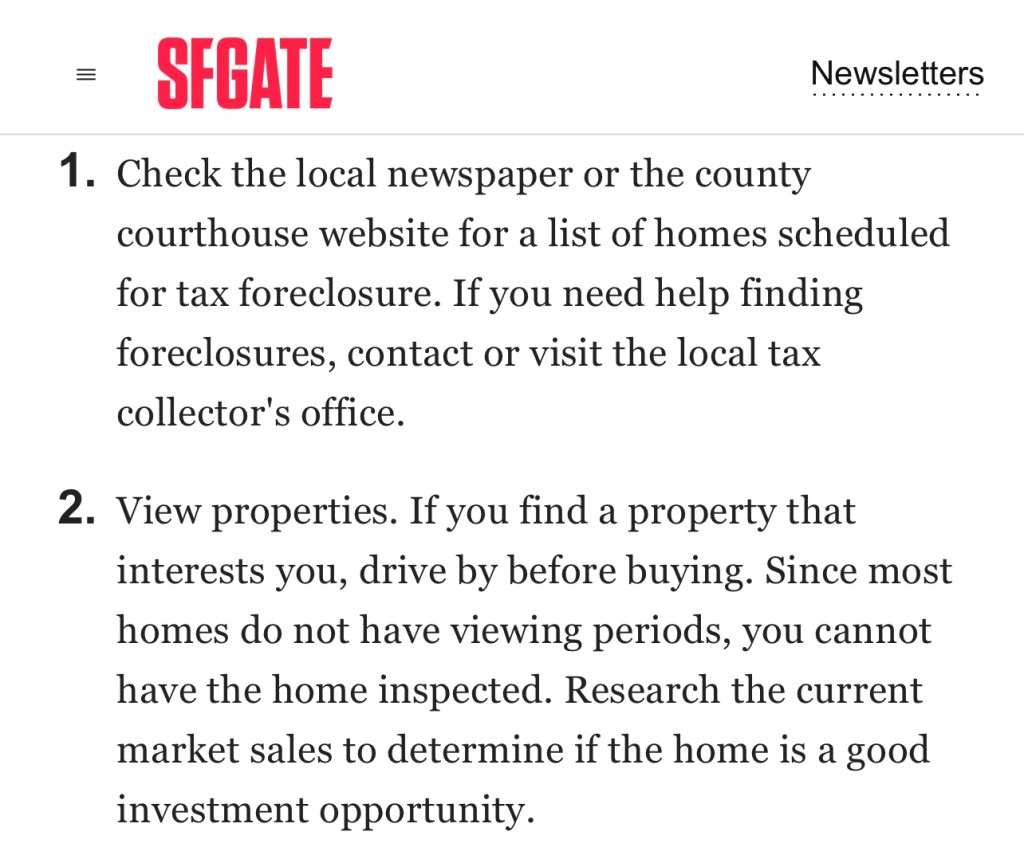

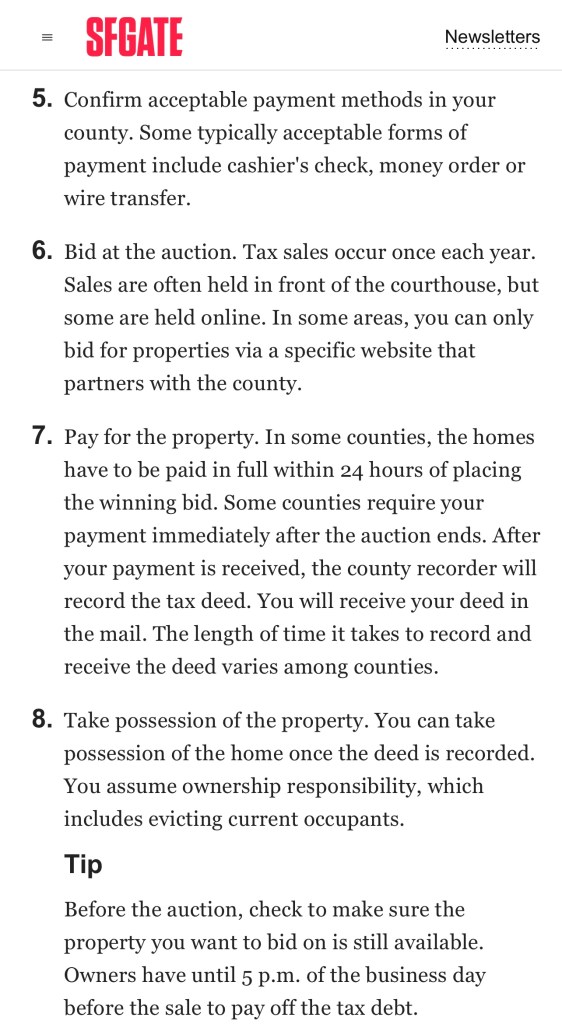

This is just a quick overview but basically you need to look for upcoming foreclosures in your area that are published in the newspaper or your county courthouse. Do a Google Search and research tax foreclosures and your area because you’ll also have to register for the auction before being able to bid. Most auctions require some paperwork to prove you have funds and deposits down before you can attend. You need to be able to pay for the property if and when you are the winning bid. Keep in mind too, foreclosure and tax auctions have rules in most places that you cannot immediately inhabit them or begin renovations because there is a grace period for right of redemption of the current owner. There is also a processing time for changing over deeds and funds, etc. You may have to wait a full year before being allowed to renovate or move in so do your research and pick up some great books. Here is a quick guide from SF Gate.

This has nothing to do with marital status or financial situation. Every woman needs her own savings account. And you need a real account that actually earns you interest. Your standard savings account at your walk in bank isn’t giving you much at all. You’re earning pennies on the Benjamin instead of the dollars you can get from a high yield savings account HYSA from well-established instiutions like SoFi. I opened a free account with them, it didn’t even have a minimum requirement, and auto-enrolled my direct deposit of my stock dividends, royalty checks, company paychecks, earnings, and rollovers. We also did this for our kids. When they turn 18, they’re going to be set for a home once they have a stable job to get approved on their own. When you open a SoFi savings account, you automatically get a free checking account too!

This is not an ad for them. I legitimately did my research and their ability to withstand the market was the top reason I chose them. Small local banks are great for your bill checking account but for savings, get a strong and longstanding bank that can survive. Think 2008 and 2020. There are a couple of other companies claiming to pay out more until you read the fine print and read their average customer payout is actually closer to SoFi and also fluctuates more than SoFi does. Upon many hours of reading and Google searching I also found articles and interviews from the other competitors’ CEOs and he even admitted their volatility during the banking crisis and if it happened during COVID, when the interview took place, they would not have survived. The company does offer home and personal loan programs but not nearly as many viable programs as companies like SoFi because they’re smaller and just don’t have that market share; which is also why their average customer is signed up a whole percentage under their advertiesed APY.

Researching more about FDIC laws and some of the provisions the CEO mentioned gave me more pause. We all know when a bank is failing, the government always does a “bailout” process as per those guidelines which are decades old. Again, think 2008 and 2020. Those are because the laws require the Feds to perform an oversite and dig deep into the insitutions financials. Why did they fail? What were their reserves before and after? How are they being spent? etc. That’s what is happening in those bailout meetings with presidents because FDIC doesn’t just pay out–and that is why I also chose SoFi. Banks that have far less reserves and profitability, as this other CEO admitted his HYSA did, they have far more regulatory procedures to go through to get that money back to customers. That takes a lot of time which means your money could be MIA for an extended period of time while the bank undergoes federal scrutiny and forensic accounting audits. SoFi doesn’t have that problem and in a crash, is far more likely to have your money available. Done deal for me.

HYSAs work exactly the same with one caveat which is also a federal requirement so ALL US banks follow this rule: Limit 6 transactions per month. However, you can open as many free accounts as you want! You can even open a dozen at once and name them. For example; mortage, bills, college fund, etc. I signed up on my phone in like 5 minutes and just put in $50 to start because I had to make dinner and setup my deposits after I put the kids to bed.

This is a sticky subject but the reality is not all women are in marriages where the spending and savings duties are equal; or a healthy situation currently in their marriage. Some women are even in a position of working to put themselves in line to leave their spouse, match their income, have their own accounts to alleviate the stress on their household finances, or even escape an abusive relationship. While it’s not a pleasant discussion for many, it’s necessary for many as well. So let’s get into it….

As someone who has been in this same circumstance before, the reality is working in some fashion is essential. I wanted to escape an abusive situation but I had a newborn, no car, and recently had to move far away from small town transportation and means of getting to a physical job. I had a choice to make. I got a stroke of luck that helped me.

I had turned on the TV one day and The View just happened to be on and beginning that second was a segment on work from home jobs that were legitimate careers to start with no education that I could try. One resonated with me but I will share a few here. I never watched this show but I watched this episode the rest of the show because it was divine intervention for me!

One suggestion was working as a freelance writer. I loved writing for hours into the night and I’d often been told I was a great writer….but could I use it as a tool to make money every month to feed my baby, buy diapers, save for a car, and move out on my own to safe environment by the end of the year; or sooner? I immediately tried the websites they recommended. At the time, those sites were called Elance and Odesk. I ended up doing well! I made more than minimum wage at least and neither of us starved. I did get lucky that my parents let me move in with them and got me a beat up old car to at least work a second “real” job as a night manager at the hotel one mile down the road. That job allowed me to work a lot with my freelance career simultaneously.

I wrote articles for everything from hemorrhoid creams to tractor trailer marketing ads, to ghostwriting horror short stories, and websites for bloggers and their websites. My very first job was actually a celebrity gossip columnist. I didn’t give a damn about celebrities and gossip is ridiculous but I had a new mouth to feed and rescue. Within an hour of signing on, the news broke Farrah Fawcett had died. I got to work. Four hours later, Michael Jackson did too. I wrote articles and updates every hour as those stories were evolving and filled my 20 article quota for the week quick! When I ran dry on ideas, I thought of every C grade celeb I could and did a “Where are they now” segment. I eventually got better gigs in fitness and writing medical articles for doctors. I even ended up writing articles on the NFL, on my own for fun, on the Indianapolis Colts because my favorite player was Peyton Manning and CLEARLY we were poised for a Super Bowl run! We were. We lost..but we did make it to the big game again, losing to the New Orleans Saints. I had no connection to Indianapolis. None. Nadda. But I loved watching him play and I was fired up to see him win another championship. I joined online chat groups on fan sites and their media team took notice of the full length articles I was writing. Eventually they were being featured on the Colts website on the front page with my name in the byline. I used that recognition to beef up my resume and expand my reach to potential editors. It worked and I did more in sports and nutrition.

I started feeling brave and ready to dive into writing books, children’s books, because my son was a toddler now and I loved making up stories for him. I started a Facebook account and began searching pages and groups to find people who wanted to be authors too or already were getting their foot in the door. Literary Agents weren’t quite warming up to my stories so through research and finding like minded people, I made the dive into self publishing, a third stream of income for me, with my freelance work and “real” job now working at an assisted living center. I had no experience there either and no child care one day when I saw they were hiring. They didn’t require a degree so instead of not going into apply because I had my baby with me alone, I sent a resume with a kind letter as professional I could, explaining my desires to pivot from dead end jobs, help people instead, and my ambitions for the future that weren’t related but showed my eagerness and motivation as an employee in general. I got the job. My self published books weren’t selling much at first so I needed this and my freelance gigs to keep going and pay bills. Eventually, those books and more in adult genres like crime and historical nonfiction would pay me residuals every month.

For anyone reading this, you will have to create opportunities too where there aren’t any. I had no education or experience in anything I wanted to do. I created a portfolio of pieces based on the job listings I saw every week so even if I didn’t get what I applied for, I was building my portfolio. Every company and editor wanted 3 samples of work so I created as many as I could in every industry I saw. I researched like crazy to learn enough to get the jobs and be knowledgeable in my articles. Then, I found better and more lucrative ways to work from home that were inexpensive to start and paid really well!

By this time, I’m married with a baby on the way and I’m working at a veterinarian office because I walked in and asked if there were any volunteer positions available because my dream was still to go to college and work with animals. They gave me an unpaid internship on the spot and eventually I became a vet tech! I was also working at Macys as a sales agent and worked my way up to a specialist with Ralph Lauren. Everyone started calling me Rachel which I actually loved, I won’t lie. I was also getting married so money was finally not an issue anymore. The problem? My doctor wanted to put me on bedrest and I also wanted to stay home for at least a year after my second son was born. I would not be returning to either job and I wasn’t working much freelance anymore. So, I needed something else.

One of my very loyal customers at Macy’s was a real estate agent and she really believed I had the personality, drive, and ability to start a business from scratch and be successful. So I did! After my son, was born, during feedings and naps, I would study for my real estate course. I only needed twenty hours to take the licensing exam. The whole course, books included, was $250. I aced my test first try and found a local brokerage to who took me on and I was off. I started slow but eventually found success with Instagram, blogging, sending mailers, and getting better at meeting people to do okay for six years before moving to New York full time. This career gave me the ability to make good money, work my own time, be with my kids, and when my daughter was born (3rd child) I worked night and day to study for my national lending exam so I could work remotely from home with her after she was born. It was cheap and fast like my real estate program. Fast forward to 2024, and I will be licensed in multiple states as an agent and lender while working from home and making a high income.

Why the life story? To tell you how I got here, created my destiny when it was bleak, kept striving for more without degrees and money, and how I found my own path to ditch bad relationships and make my own way without my husband to fall back on or an abusive partner who would have surely killed us one day soon. Money is the biggest killer of marriages; arguing over spending, who’s contributing more, husband very controlling of money, financial abuse, or the woman needing her own income and accounts to leave without him having access to.

I encourage women to do what I did and look at their STRENGTHS, even if it’s not your passion, to what can you profit off of. Think about people on local Facebook groups offering to do mobile detailing, yard work, dog walking, etc. Can you strap a baby on you and walk or take transit to those places and restart your life? Do you have crochet or custom cake and cookie skills people will pay to have at their parties or just for fun and order? My son did oil changes at 15, made easy custom cutting board shapes, and other items for cheap for a profit before he could be hired by law at a job.

What passions do you have? Do you crochet, write, paint, photography, etc that can be sold locally or on Etsy? What could you learn in a few months to do? Any of these? Maybe real estate too or becoming an insurance agent? Virtual assistant? Maybe you’d be a great influencer even. These days, affiliate marketing, drop shipping, content creation, and more are allowing you to work just from your phone and make monthly income that is stable and legit.

For some more ideas, go to Pinterest and just look around for “Work from home jobs”, Side hustles”, “Things you can sell”, etc and go down the rabbit hole of suggestions. Something will speak to you! You are not alone and millions of us have been there, or are, and we are here for you. If you ever need help, always call the national hotlines for domestic violence, your local battered women’s shelter, and other resources. Google can help you find dozens more near you and nationwide support. Get the help you need to be free!! This time next year, could be so much better and happy. You deserve it and I will help you get there. I believe in you wholeheartedly. Message me anytime. ❤

What should you be doing right now to get out of the rat trap you’re in? The rat race is what most of us are in but sometimes it’s worse than that (been there many times) and you need to dig deep to pull out pennies even. How do you break that cycle when you’re ready to rejoin the race and win? Here’s how:

For starters, get yourself a High Yield Savings Account and use that instead of your regular savings account (which is paying you zilch in interest) to earn nickels on the dollar instead of a penny. Yep, there’s a big difference between an HYSA and the one you have now. They’re both free and usually have no minimum balance requirements so ditch your old one.

Secondly, and don’t hate me, but streaming is getting so expensive lately. Do yourself a favor and ditch one for good. Instead, put that money every month on autopay into your HYSA instead of your credit card. That’s a savings bonus right there!

Third, what is your highest recurring debt? Is it your student loans? A car payment? A credit card you owe too much on? Pay an extra $50 onto your minimum payment (or whatever you would usually pay on it) and do that until it’s gone.

Fourth, if you have retail credit cards, stop charging on them. I’m talking Macy’s, JCP, Nordstroms, etc. I know the holidays are around the corner but people tend to overspend on these and not only do you buy more, you pay more in interest because you’ll be paying for years on all these over expenditures. Those sales will end up being more than double the price you paid! That $40 discount will be at least $75 OVER sale price by the time the interest is paid; if not substantially more. Don’t do it! Pay them down and let them sit. Don’t cancel them. Just let them remain at ZERO.

Lastly, actually track your spending every month for Target, MCD, Starbucks, fast food, shopping, etc. Knowing your numbers is key to success and set a goal each month to reduce that number by 10% the following month. You spent $600 at Target this month that wasn’t all food and necessities? Spend no more than $540 this month. Then keep reducing until you get your extra spending under control and have a savings building up.

It’s a new month so let’s set new goals and expectations!