This is one of the most old school tricks in the books 📚 but nowadays it seems it’s not commonplace anymore. It’s a shame! This is basically a way to pull money 💰 out of thin air and pay 💰 over and over again. But how can that be?

Think about when you buy a home. Do you actually have the money the home is purchased at? Usually no. You finance it because that $550,000 asking price is not what you have in that bank but what you are approved for by a lender. The same is true in the #brrrrstrategy method; except with #brrrr you ALSO get the money 💴 you are financing in a lump sum! Plus, remember you are renting it out to get the #cashoutrefinance paid off. You basically get the house for free AND you get way more back in a refund than what you paid for it. That cash 💷 back can be used to pay 💰 off student 👩🎓 loans, 🚘 payments, your mortgage 💸 on your own home 🏡, or anything at all. It can be just sitting 🪑 in the bank 🏦 in an #hysa account earning interest up to 25x the rate as your current savings account. It’s up 🆙 to you!

For more information on this, I have a beginner course on #realestateinvestingtips and #realestateinvesting with traditional financing methods and a guide to those loans; as well as how to leverage your own home 🏠 to do the same thing as the BRRRR Method. DM to get the course! It’s only $25 and available for life.

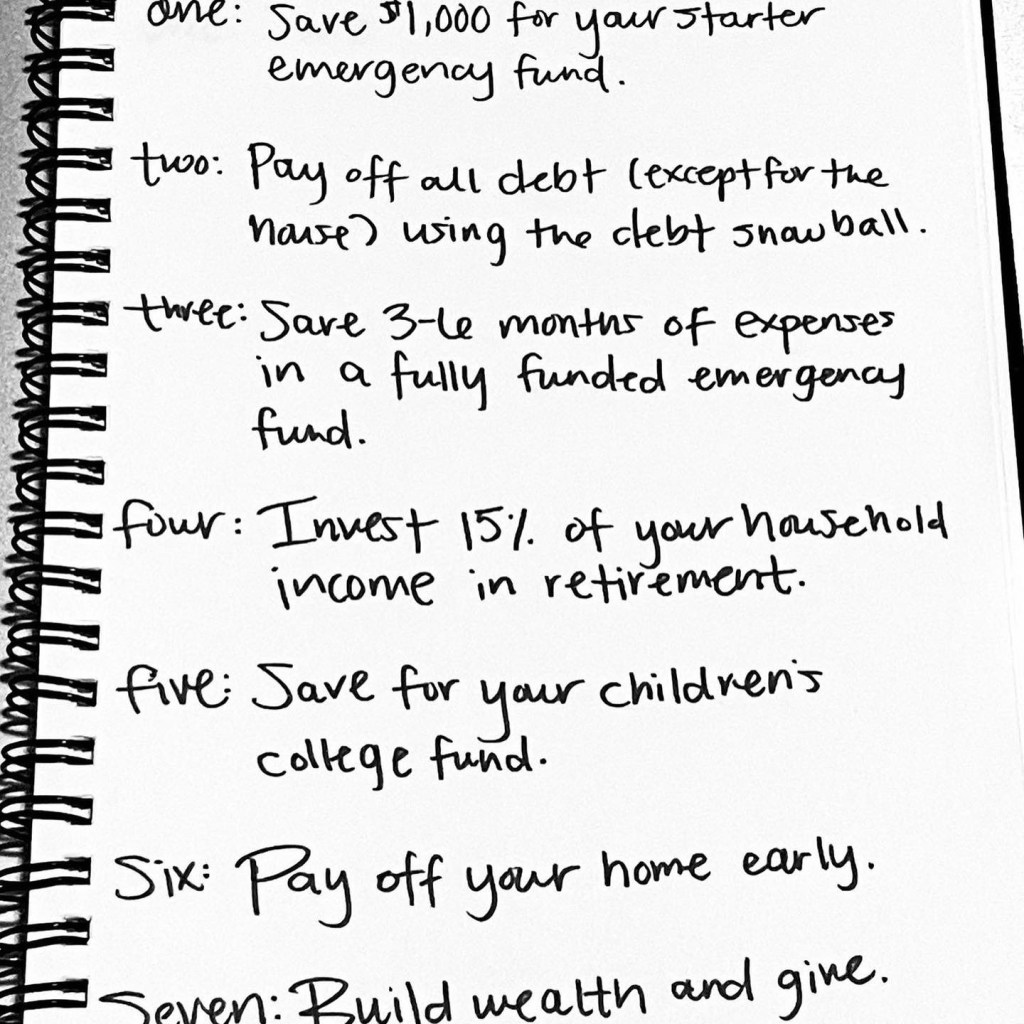

Dave Ramsay’s plan (swipe) and mine. I don’t disagree with his but he doesn’t explain how to save and invest or build wealth and that’s what so many gurus do. Here’s the thing:

The number☝️ way to expedite your journey to a bigger 🏦 account is to reduce how many bills you pay; mainly cars and 💳. Reduce credit cards 💳 to under 30% of the max limit at most and pay an additional $50 to your car payment minimum each month. Same with the mortgage or make a separate $150 payment to your Principal Only as stated in the memo 📝 line.

Number ✌🏼 is to make your money 💰 work as much as you do. Put at least $100 into savings each month in a high interest savings account that pays up to 25x what a normal savings account does.

Number 🤟🏼 is to make your home your income. Seasonal and vacation rental income are one way as is renting it out when you are moving, refinancing to remove PMI and/or reducing rate, HELOC to purchase an income property, BRRR, etc.

Number 4 is to involve your kids in it too and teach them how to do the same.

Number 👋 is to put money into a RothIRA and have one for each child.

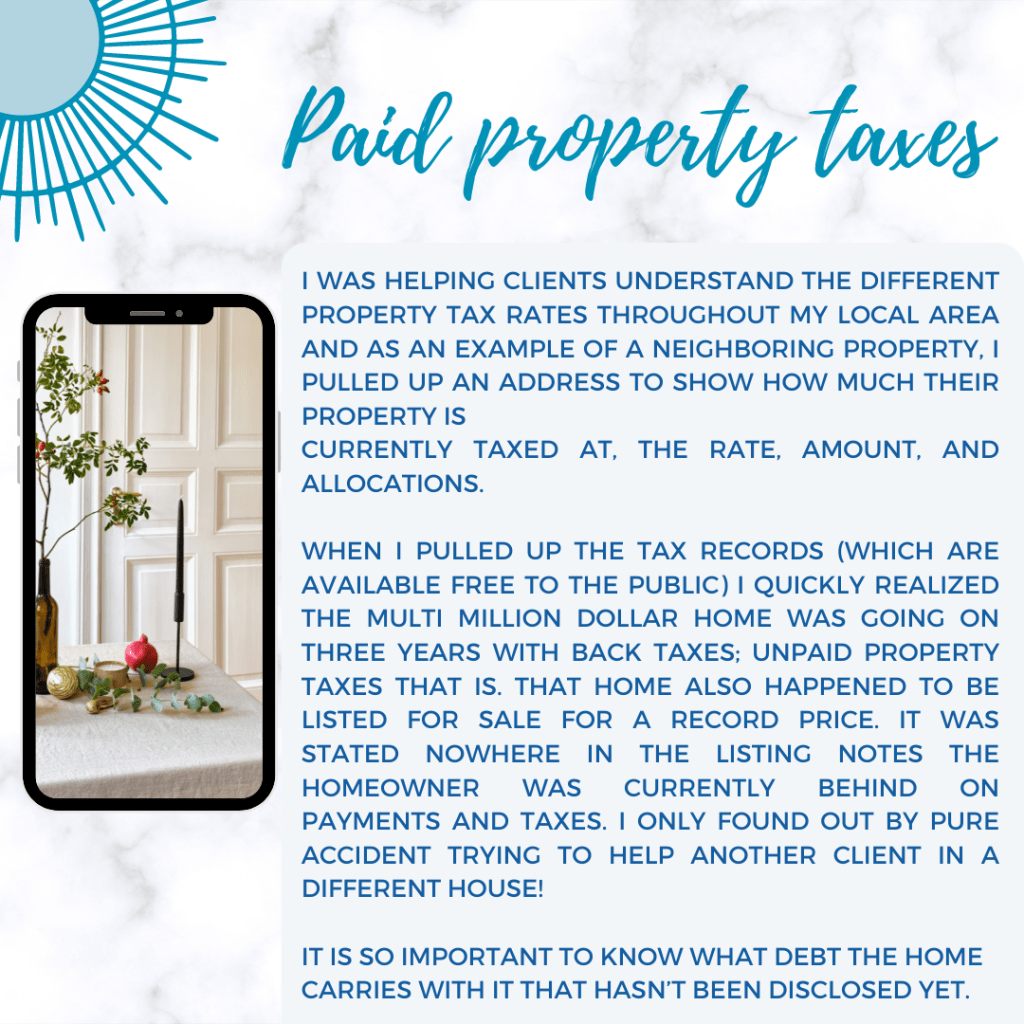

We all know about closing costs, down payments, escrow and lending fees, etc; but, what about other expenses hiding in your next home’s history?

Here are 3 costs to check on right away and why you should request your agent pull a preliminary title report (prelim) from their title rep at time of offer or consideration of one.

Bookmark this post!Are they paid or behind? Those costs MUST be brought to current before transfer of ownership. Someone has to pay up.

If the home is behind on property taxes, the county registrar will need those liens to be cleared before recording the deed. Liens are recorded with the county as well and liens have priority; tax liens always go first. If the owner is behind in payments and other finances as well, the home sale has at least one more lien, the actual mortgage loan balance, that also has to be paid immediately upon sale.

If there are no additional funds left for them to cover, in order for the sale to go through, you as the buyer could be on the hook for that money or let the deal fall through if it’s not agreed in the contract to pay the balance. It will be thousands to bring the home to current on liens and pull the owners out of debt at sale.

Not an out of pocket expense you might have been prepared for without a prelim but one you might be asked to help with for the sale to complete.

HOA dues are also a priority lien and are due upon sale

Last year our local paper wrote an article about a woman who lost her home to an HOA lien (I believe she owed about $15, 000) that she couldn’t pay due to immediate job loss as a result of the pandemic. She owned the home OUTRIGHT. Free and clear. No other debts were attached to the property and her home was long paid off; yet it was auctioned off anyway and she was given a 30 day notice to vacate from her home of over 30 years that she had no mortgage on. Why? Priority liens need to be paid! You cannot continue to live in a community you are not paying for and the land isn’t entirely owned by you. You also shouldn’t a paid off home as no debts!!!

When a home goes for sale, the HOA will pounce even faster, and the county records will show in a title search the home is in default for such an amount and to whom. If the owner refuses or can’t pay, the buyer must in whole or part to save the deal. Otherwise it goes back to market and you have to restart your home search. It can be another expense of thousands to pay off; even if both sides split the bill if you do offer to put towards the balance due.

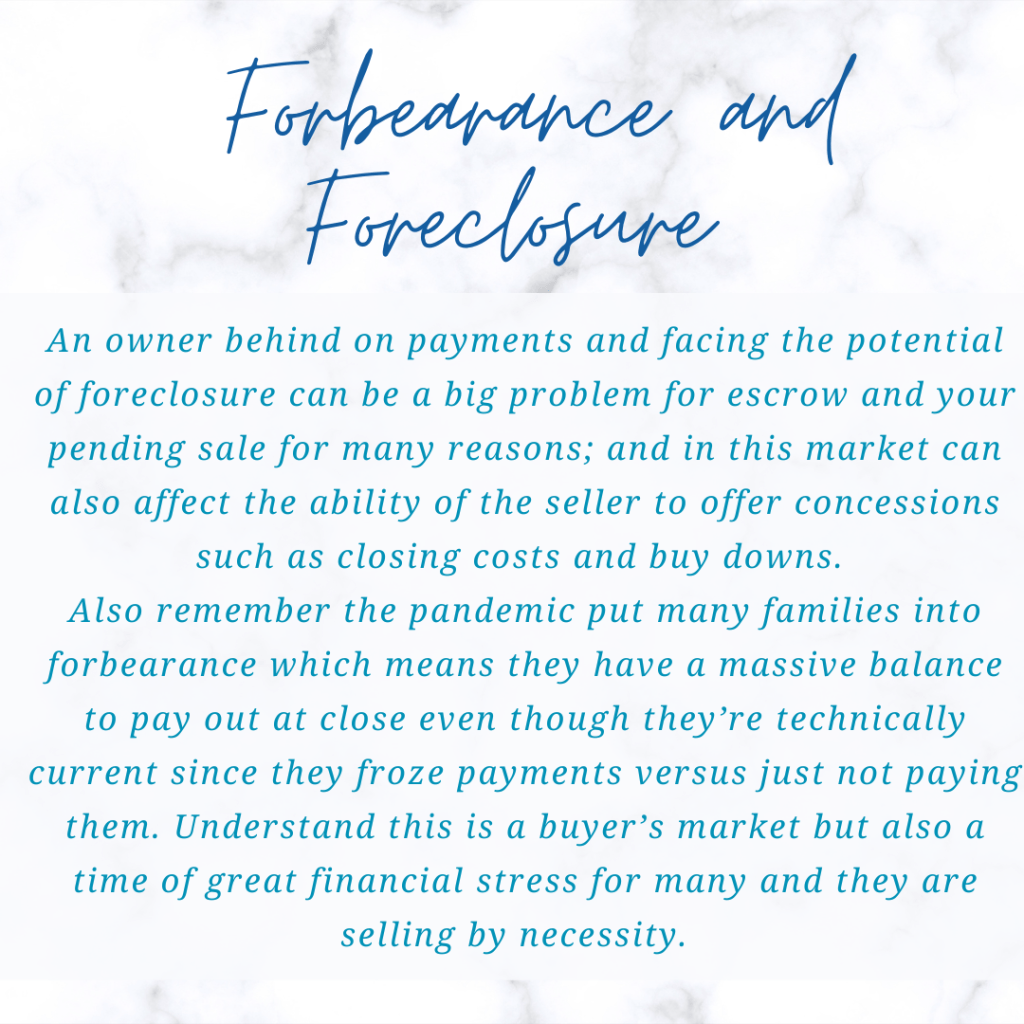

This is a tough one because it is a common and sad problem. Think back to post 2008 and now the last two years. Those who weren’t buying may not have been able to because they were losing their jobs; and, to save their home waiting for the world to restart, decided to put their home into forbearance as many mortgage companies offered; but the problem with that? When the forbearance period ends, a massive payment is due. The entirety of the payments you skip become due AT ONCE. Most people can’t do that so they decide to sell instead, sometimes people bust their butt to pay towards it, but whatever is outstanding must be paid in full. To do that, many are forced to sell before their forbearance becomes a foreclosure. Then you lose the home and the equity payed back becomes significantly less, six figures less.

Be aware that again, someone has to pay that forbearance and it’s the seller’s responsibility so if they have agent fees, selling costs, and a forbearance balance, they may not be able to negotiate much, paying closing costs, offer incentives, and may even request help because of all these mounting costs and little equity; despite this buyer’s market; which could be thousands from you. Again, someone has to pay at sale to transfer ownership.

Sellers and agents are learning in this new market that first time buyers in particular struggle to understand what a rate Buydown is and how it benefits them; often choosing a price reduction over a Buydown thinking it’s saving them a lot of money. It is but not nearly as much.

Before you negotiate, read this article!

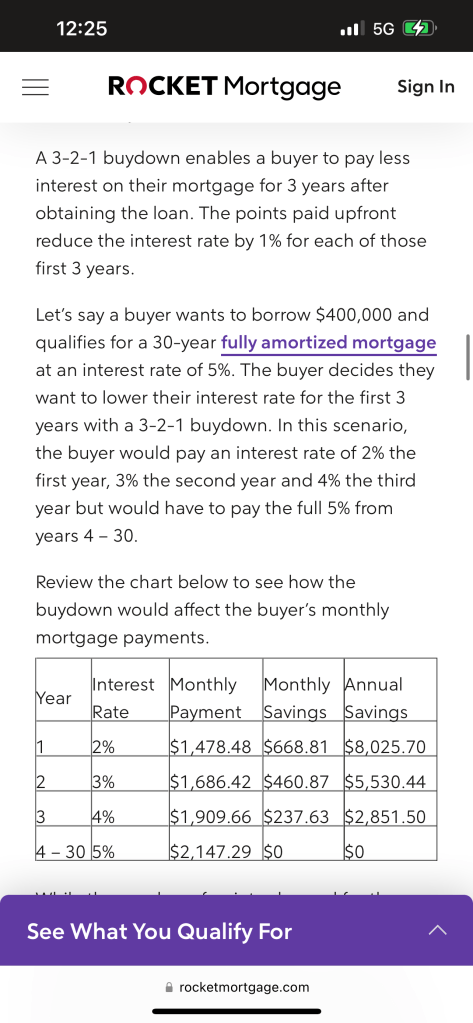

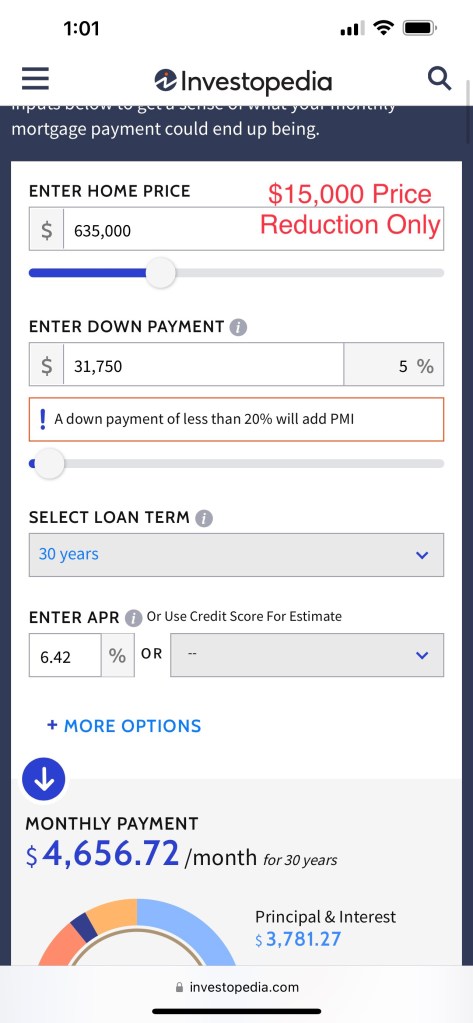

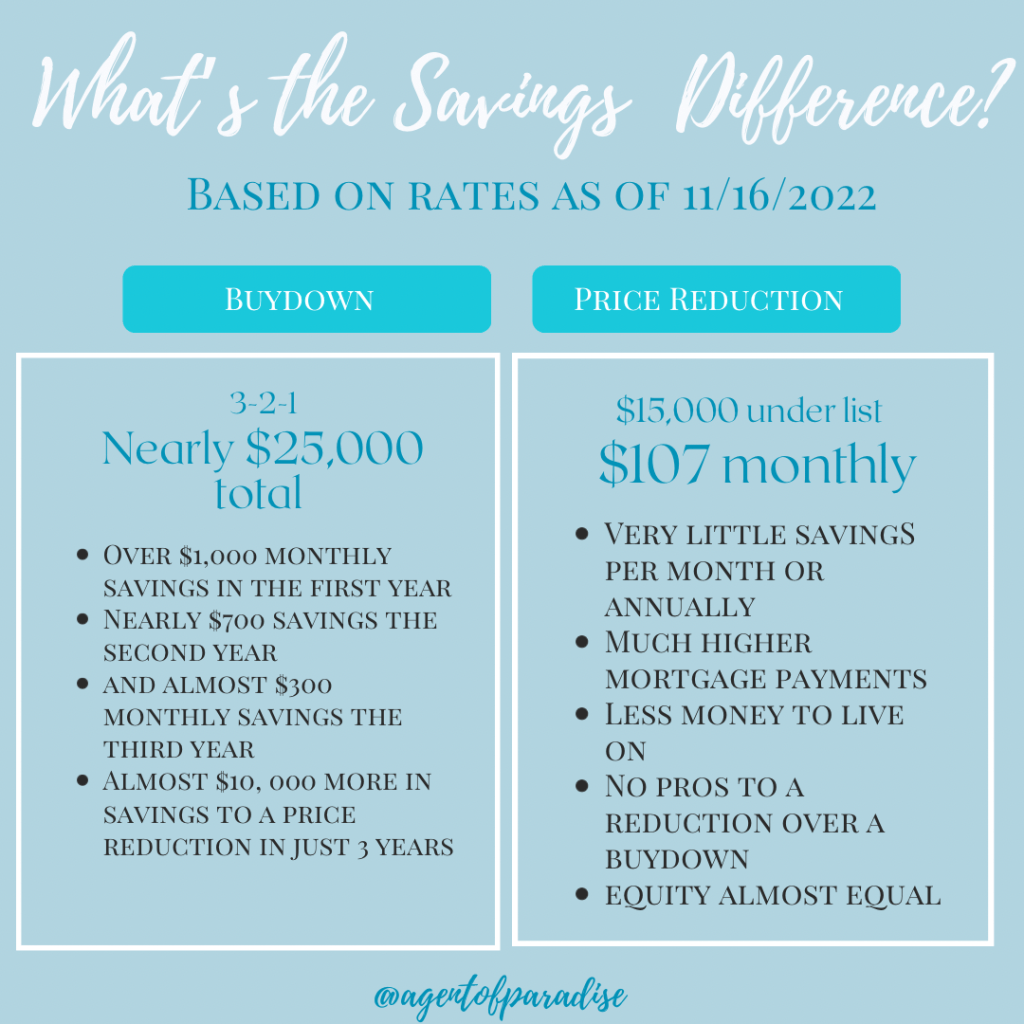

There are 3 main types of Buydown scenarios but the two buyers need to know are the 2-1 and 3-2-1 programs. These are what actually save you money on your mortgage and over time because rates are what drive a mortgage payment so high; not sale price as I have mentioned many times before. Taking $15,000 from the seller towards saving money on interest will lower you payment a lot while a $15,000 offer under list won’t save you much at all. So when your monthly payment is significantly lower every month it gives you a greater quality of life and ability to put money away. It puts money back in your bank account.

Most lenders offer this program right now so shop rates because many local lenders are best.

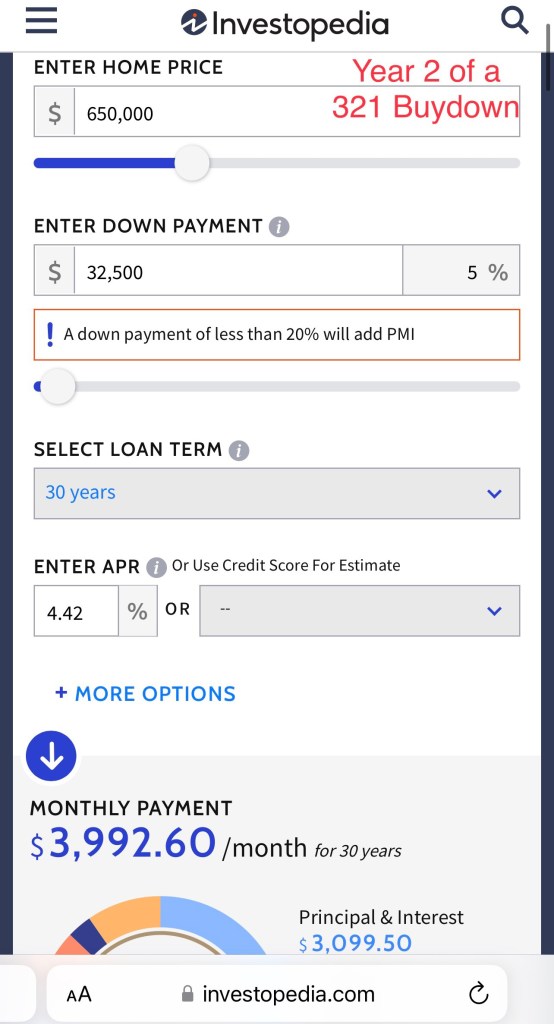

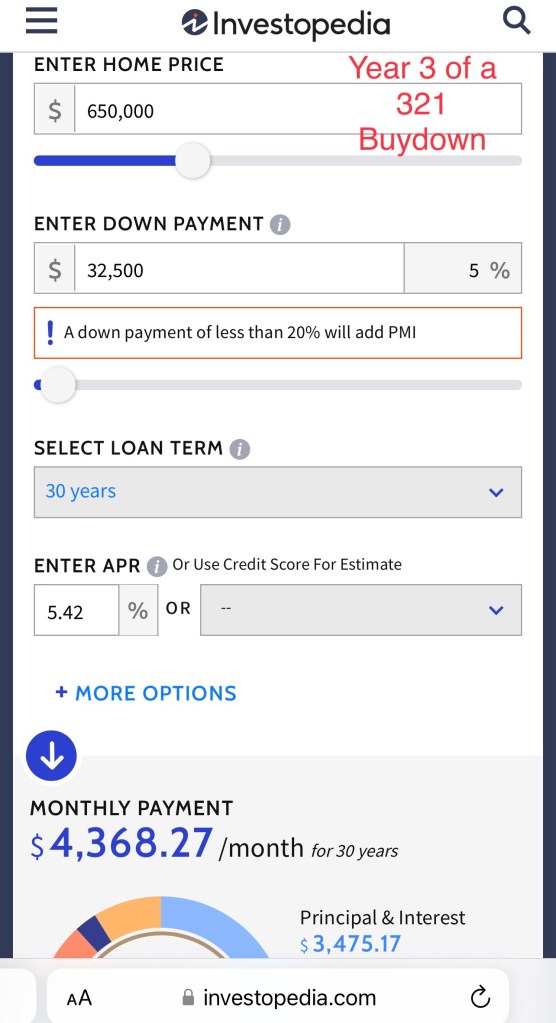

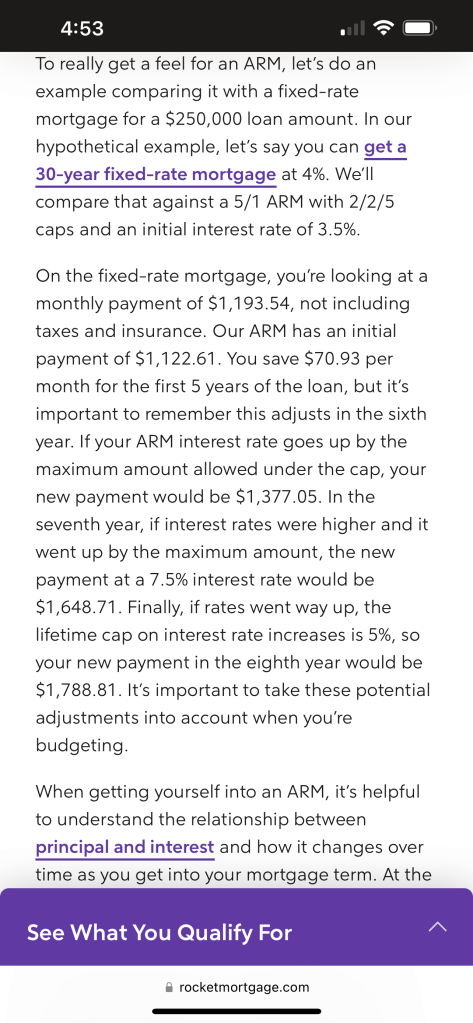

A price reduction of $15,000 will only save about $107 monthly while $15,000 for the lender to Buydown the interest rate up to 3% from current rates equates to a monthly savings of over $1,000 each month in the first year of buying the home! In one year alone you would save over $12,000 on mortgage payments!! That’s like a $12k raise. In your second year you’d save nearly $700 each month on your mortgage. That’s an additional savings of over $8,000 that year! In two years you have already saved over TWENTY THOUSAND DOLLARS on the same loan and income!!! Your third year would save you over $3,000 that year!! If you added the exact savings in the first three years from a 321 Buydown it would equal very close to a SAVINGS OF $25,000!!! So you save $10,000 more than a price reduction in the very near future after purchase AND after three years you can even refinance to lower rates again if Refi rates have dropped since your home was purchased.

Year One snapshot of your estimated mortgage payments based on current average rates Year 2 Snapshot of your monthly mortgage payments Year 3 snapshot

The savings are endless and this is why agents and lenders won’t stop talking about Buydown programs. We’re not selling you BS. We’re saving you tens of thousand for FREE!!! You essentially got a great raise by buying a home and it was paid for by a stranger just desperate to move. You can also do just a one or two year Buydown for a little less money from the sellers if they won’t put forward the $15k-20,000 needed.

If you got a price reduction instead of a rate reduction.Article Recap

If you’re a buyer looking and you are still confused or need more additional information on how this works and why it’s far superior in savings to negotiating a sale price, make sure you give me a call or text right away so I can further explain how it works and show you more math examples why it’s better to get the money as a rate reduction versus a price reduction. One saves twice as much nearly in just 3 years. Contact information below.

Contact Additional information Rules from one of my lender friends

Agents spewing this are missing the mark of what they’re trying to say….which isn’t much.

Why are agents saying this and why are they wrong? First and foremost: unless you just randomly decided to spend a $100k for a house it’s automatically FALSE. Why does a anyone spend more than list price? Competition. Other offers. Aka the market. The going rate on a house is rising because of competition and desirability. A buyer wants the house so bad they’ll pay more than the rest AND there are numerous offers coming in to beat. That’s not overpaying, it’s paying what the market is saying is its value. 💵💵Value is determined by what a buyer is willing to pay 💵💵but agents and appraisers were so stuck up their own rears to see it because most of them had never seen anything like it; basically refused to believe it was happening; and yet it did…..for two years. That’s a market all its own. That is not overpaying that is nearly 1,000 days of consistency of buyers paying whatever the market competition is requiring of them. That’s how comps are made and how prices are set: supply and demand. No such thing as overpaying.

NEXT, most people didn’t pay anywhere near $100k over but even if they did it’s because the house was best for their needs and they will be in it for YEARS to come. Aka when they sell the market will be even more valuable then and they’ll still have plenty of equity. The average though “overpaid” $40k but STILL and WILL keep that equity and have even more a few years from now if they sell. Again, NOT overpaying. At all. So stupid what these “top” (self proclaimed) agents are saying. Third, do the MATH. 7% interest over 3% is more than DOUBLE which means a huge payment for a smaller, lesser house ON THE SAME BUDGET AND PAYMENT. Let. THAT. Sink. In. FACTS. Not BS. FACTS.

Always buy the house and pay what you are comfortable and shut everyone else up. The end.

If you’re a buyer it’s also leveraging power for you.

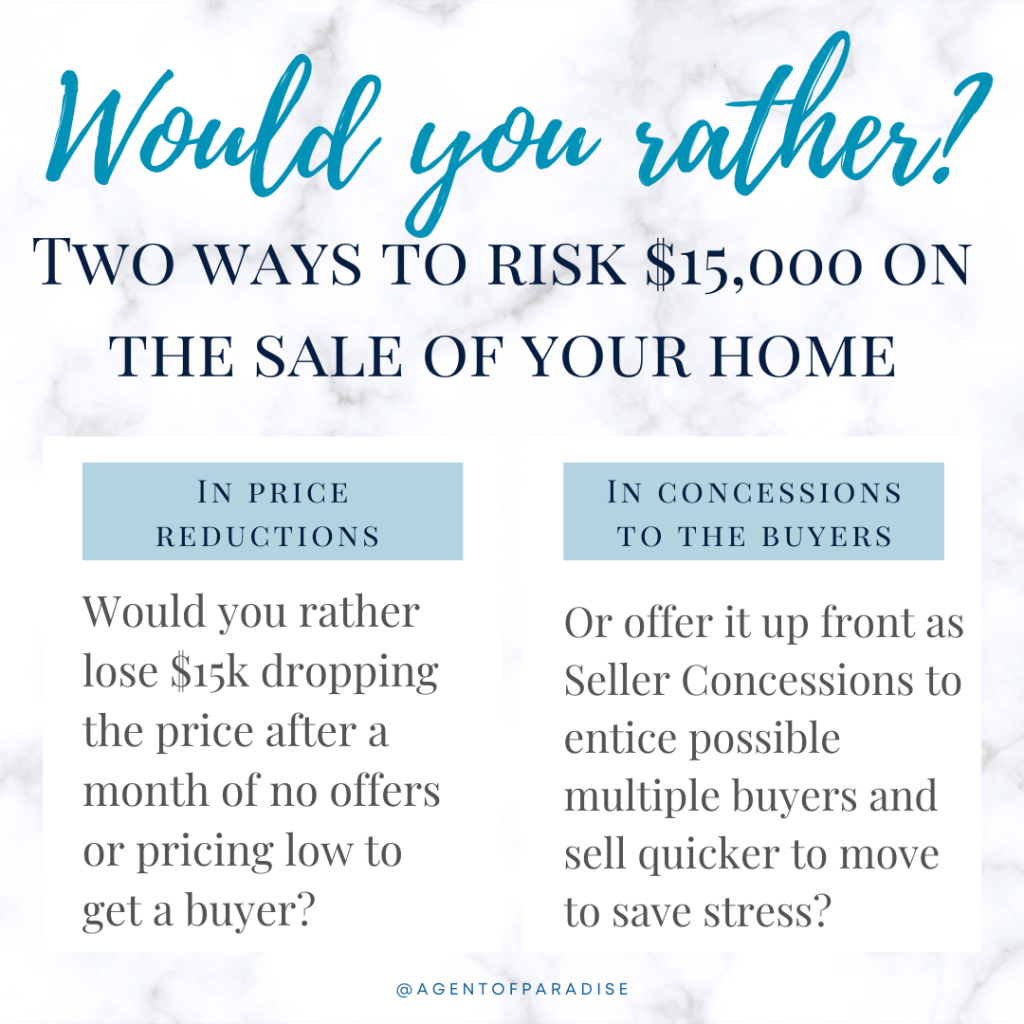

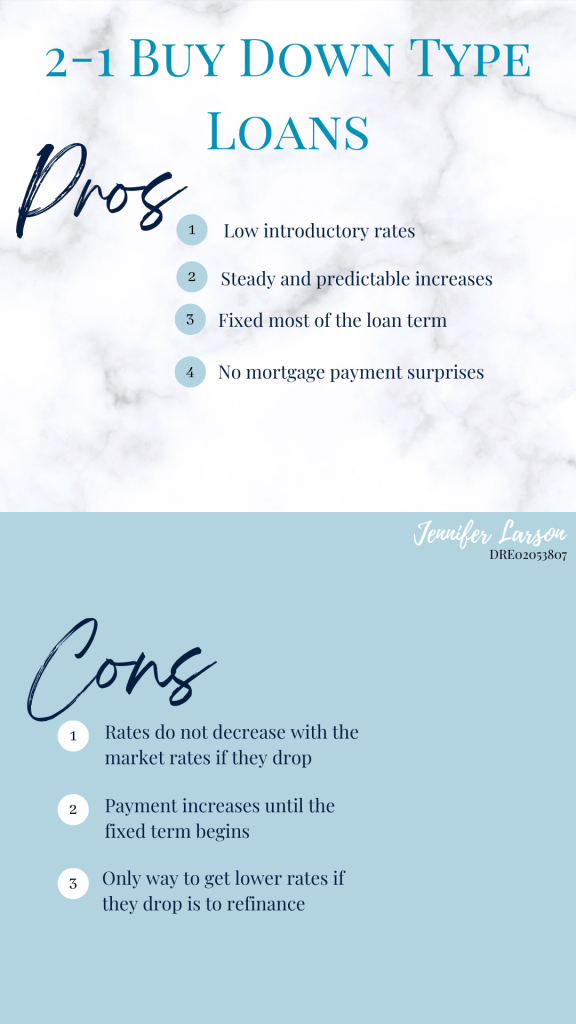

If you are prepping to become a seller in this market there are a couple of things to know as I stated in my last post. One of them is an adequate pricing strategy and enticing buyers financing to lure them in and pick your home over the competition. You can either do it to price lower or in subsequent price reductions over the span of weeks; OR, you can instantly offer in your listing to fund $15,000 towards the buyer’s lender to buy down their rate from around 7% to around 5% for a temporary buy down that helps them qualify better as well as save approximately that amount on their mortgage in just two years because they will have much lower monthly payments.

How does it work?

Lenders have a program called a 2/1 Buy Down (Temporary) that allows the buyer to either pay upfront or receive seller concessions for the cost to lower their rate 2% of the current rates for the first year and 1% off the next before fixing to current market rates in the third or refinancing if rates have dropped since then. The amount saved in monthly payments allows them better chances of approval and amount as well as monthly easing their mortgage burdens. As a seller you can help them even more by saving the upfront cost of the buy down so they truly save the money short AND long term!

If you’re a buyer you can ask for a lump sum to help buy down your rate and save money over time and each month by doing so even if you pay list price without further negotiation. It’s leverage to you and when deciding which property to go with if you need to narrow it down. Save a lot on your next home and get the house you want with more affordability. Win, win.

For more information on buy downs, I can help and get you to the right lenders. Call me!

All of these are critical to selling for top dollar.

1. Professional staging brings an interior designer to your space and turns your home into a showroom that creates a unique story to the buyer how they can live in that luxury in the beautiful home they’re walking into. Staging elevates how buyers see your home which affects price and desirability.

2. Professional photography shows off the story the staging creates so buyers swiping through Zillow late at night “Stop the Scroll” and show their spouse “look honey, we need to go see this one in the morning!” Your home staged like a magazine needs to be photographed like one. Paint the picture for buyers and put your home in the best light it can be shown at.

3. A clean home free of your personal photos, knickknacks, personal style, and oddities helps create a visual for buyer’s trying to imagine themselves as residents in the home. They need a clean and minimalist design so they can mentally move in and see how they feel when they do. Hire professional cleaners before your first showing or open house as well.

4. Don’t stop at steps 1-3 and then let buyers walk into a disaster zone, cluster fudge of a garage where you just crammed all your junk. Get a storage unit, have a garage sale, trash, recycle, donate, and give away whatever you can. It makes moving day easier too.

5. Put aside money at escrow from the sale proceeds to entice buyers to come see your home and give them extra reason to choose your property over the others they saw. The monthly mortgage savings for two years might encourage them yours is a better deal and help them decide overall.

6. From the get go, your agent should be calling every potential buyer and brokers office they know getting people in the door for feedback, marketing, buyers, and attention physically in your home and deciding if the house is best for them. A broker can see it and help share it, as well as know who else to call from their buyers and schedule showings with you. This is how you get more showings and offers.

7. Don’t price high or you will sit on the market forever and ultimately not sell or not until you do a couple of price reductions. Buyers schedule first the homes that are priced right or a little lower because they’ll be the best deal for them and want to get in before others do. You’re far more likely to get multiple offers at list price or better when your home shows well and feels like an excellent value.

8. If the home is almost ready, call your agent and get them talking to people right away. When a good listing is about to hit the market, I tell all of the agents and clients in our office and they do the same. We try to schedule showings first to beat the competition and get our offers accepted before everyone else. The first offers are usually the best!

For more information, text Jennifer Larson to schedule a call or ask questions. 760-625-6836

Today I am finishing week 3 of this #masterbathroom #remodeling at the #CasablancaNavarre project and I did a ton over the weekend.

There’s a reason tile install guys charge more to install bigger tiles. These large format tiles are HEAVY 💪🏼! I am so sore and stretching constantly but everything is coming together. I did all of the small cuts on the tub surround too so I just need to mortar those in and finish the shower tile. Then I can clean it all up and grout!!

Week 4 will be completing those steps and getting ready for the glass and fixtures to be installed then simply a fresh coat of paint and deep cleaning to stage.

The #mastervanity area also will get grouted and finished to show you later. That’s it for now. I was drenched and drowning in sweat so I changed every ounce of clothing and got cleaned up. Now I’m resting with ice water in front of a fan. 😂 Have a good day!

If you want to buy house before the end of 2023, you need to do these 5 things!

Buying a house obviously comes with a down payment typically but saving money in the bank is not the only goal you should have. The other is working on is your DTI. Your Debt to Income Ratio is by far the most overlooked number buyers don’t address. Lower your credit score is one great goal but how much money you have going out to coming in is a huge factor in the interest rate you will get and how much money your new home will cost you monthly. Rates are the biggest part of your mortgage and DTI affects both your credit score to lenders as well as your approval amount, and what interest rate you qualify for. So being a spender can cost you more than what is on the bottom of all your receipts. Saving money isn’t just for down payments; it’s for saving you money on your mortgage and lowering debts!

Each of these 5 tips to saving for a home lower your DTI, improve your credit score, help you qualify for a better home and interest rate, and save you money for decades to come. 💵💵💪🏼💪🏼😎😎

Be sure to follow me on Instagram and add me to your favorites for more tips and advice!

Bookmark this article and talk to a lender today! They actually went over 7% a couple of days ago before dropping slightly again.

Who wants to pay this much interest on top of their home costs? With rates being so dang high, lenders are shifting gears and offering up programs they haven’t in years at this level. They want to stay in business and know buyers want to save money and still take advantage of dropping prices; but how? Like this:

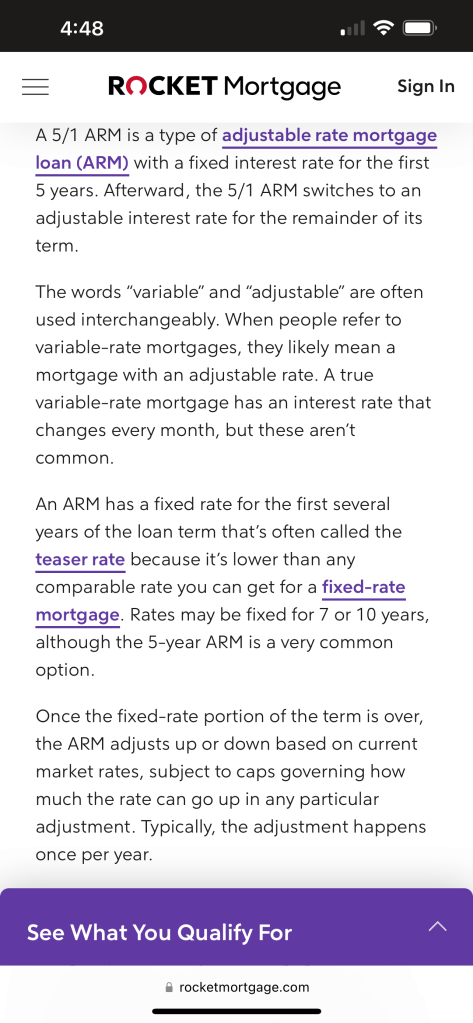

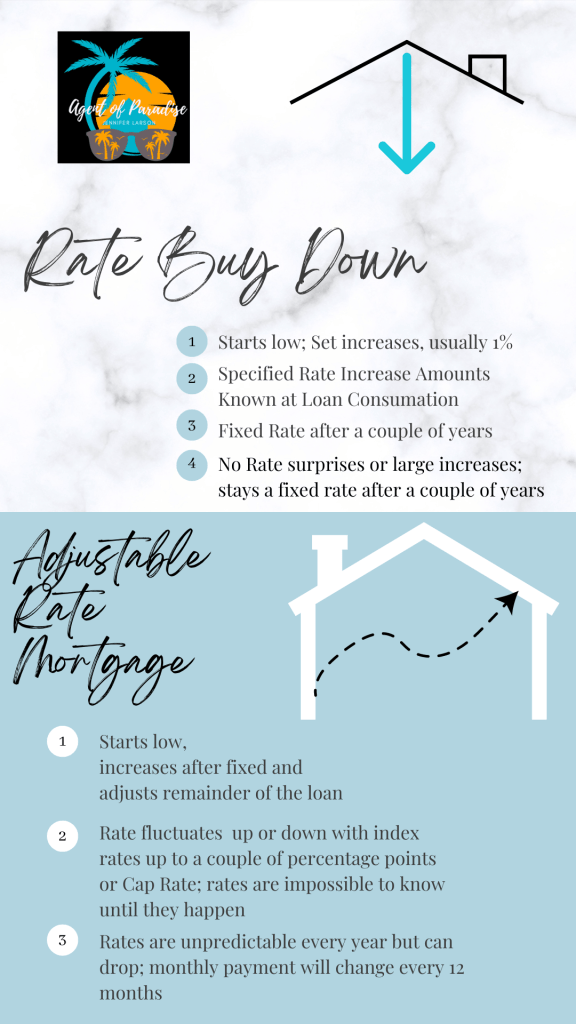

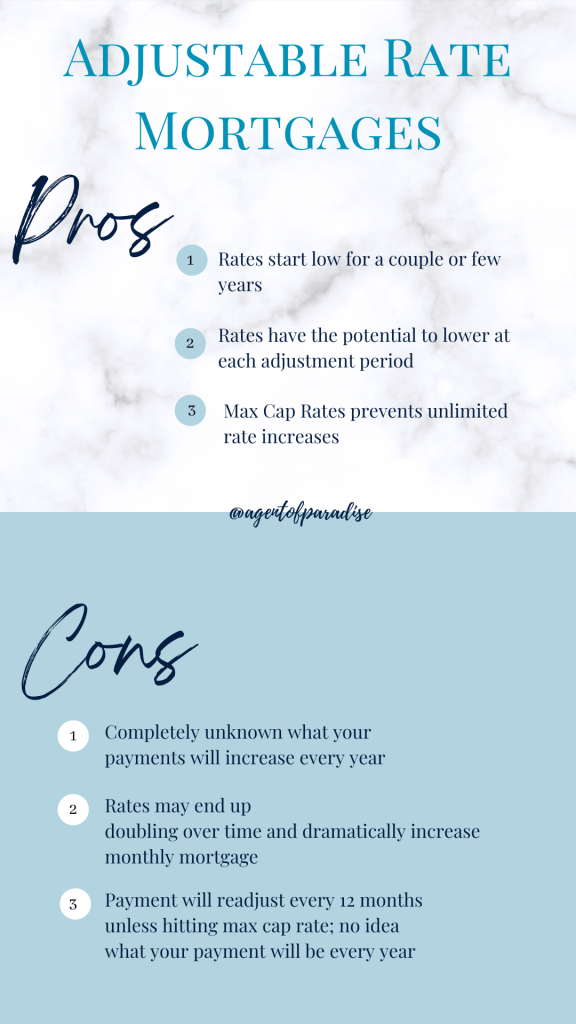

Adjustable Rate Mortgages give you a savings up front without buying down points and can be easier to get than a fixed rate loan for some.

Here’s how they work, based off indexes in the future to determine what interest rates you will pay and those will determine your new adjusted bill.

They’re not for everyone so please work with a lender who really compares all options first.

What if rates get better before my next adjustment period and I want to take advantage but my loan doesn’t adjust for a while?

Notice the last paragraph notes you can refinance to a fixed rate if rates improve! That’s the key to saving long term.

What about buy downs? Generally speaking, their up front cost is about the same as their overall savings, or a little better, but the monthly payments being cheaper and equity growing faster is what’s important to most people. They also don’t ever raise in cost so they’re a relief for buyers using an ARM loan worrying about potential rate and mortgage payment increases over the years.

You can also ask the seller to buy down the rate for you and really save!Does this best fit your situation to buy now?

Compare the two loan types side by side:

And go over the good and bad of each:

Remember that ARMs don’t have an up front buy down cost but they can raise over time up to 10% with current offerings so planning to refinance in the future is something to prepare for.

Have more questions or need lender recommendations? Call or text Jennifer Larson at 760-625-6836.