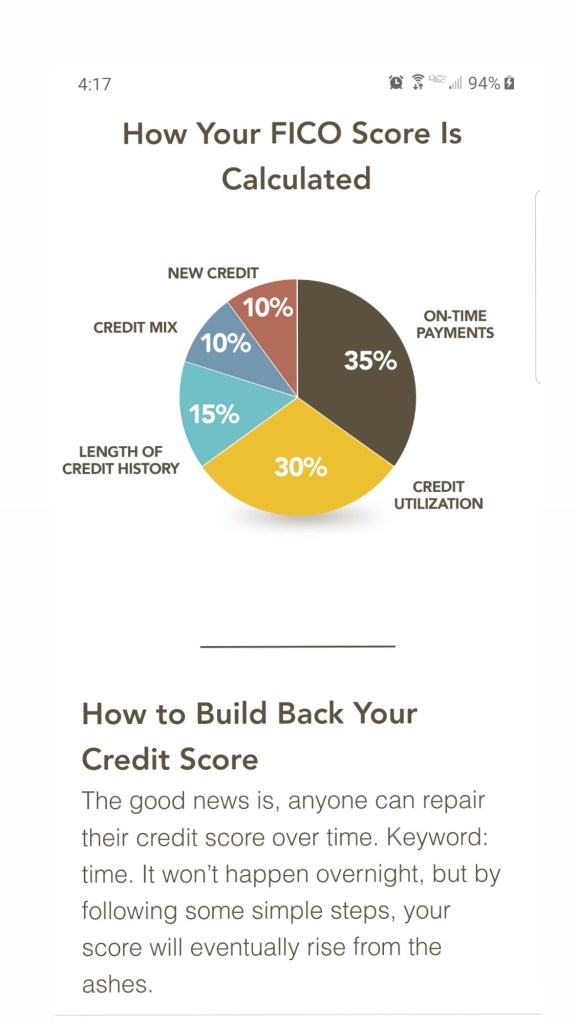

This will give you a good estimate what your payment would be when planning your down payment.Utilization is how much you USE your credit card, not just the outstanding balance.

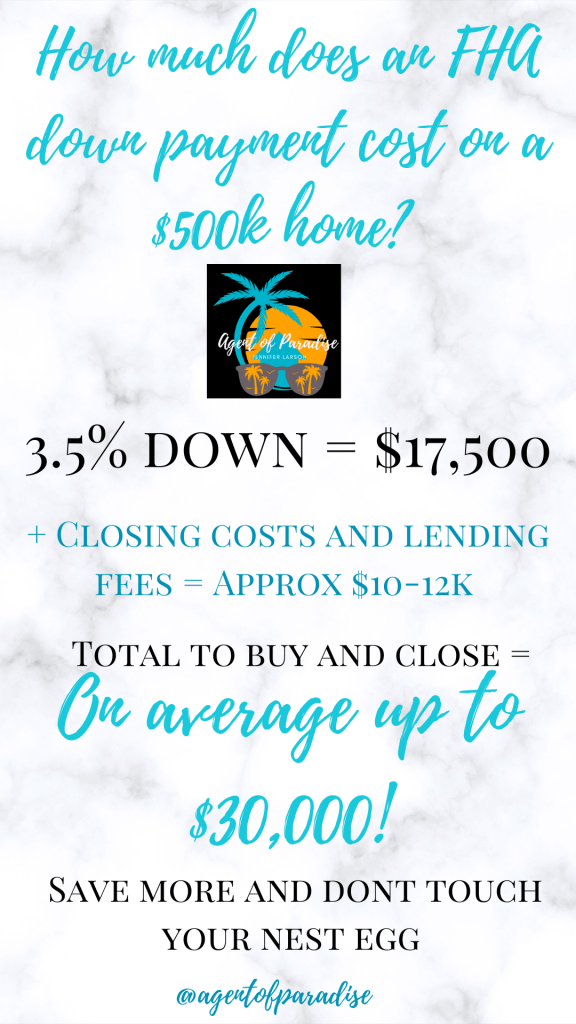

You need to know the basics of how credit and your mortgage payment are calculated while you’re planning to buy a house. Remember for your down payment you also need to account for other fees and closing costs so double your down payment needed and that’s the minimum you need to close.

⬇️ ⬇️⬇️⬇️⬇️⬇️⬇️⬇️Your lender should remind you of this as soon as your offer is accepted and escrow is opened.

This is the time to compare rates, call multiple companies, and get a policy in place because it is a requirement of your loan and for some can take longer than others. You also don’t want to forget! Get it done soon after escrow is started.

Check your annual statement for your rate.How to look yours up Look for this menu online

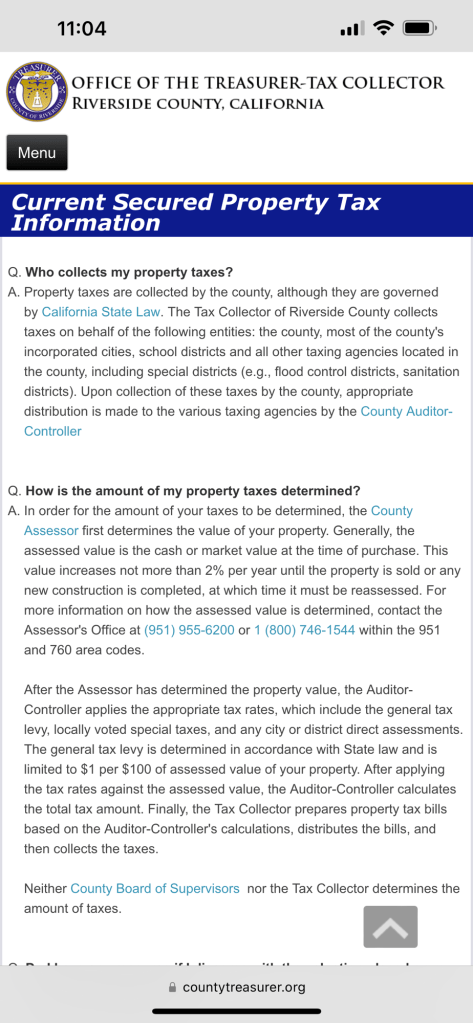

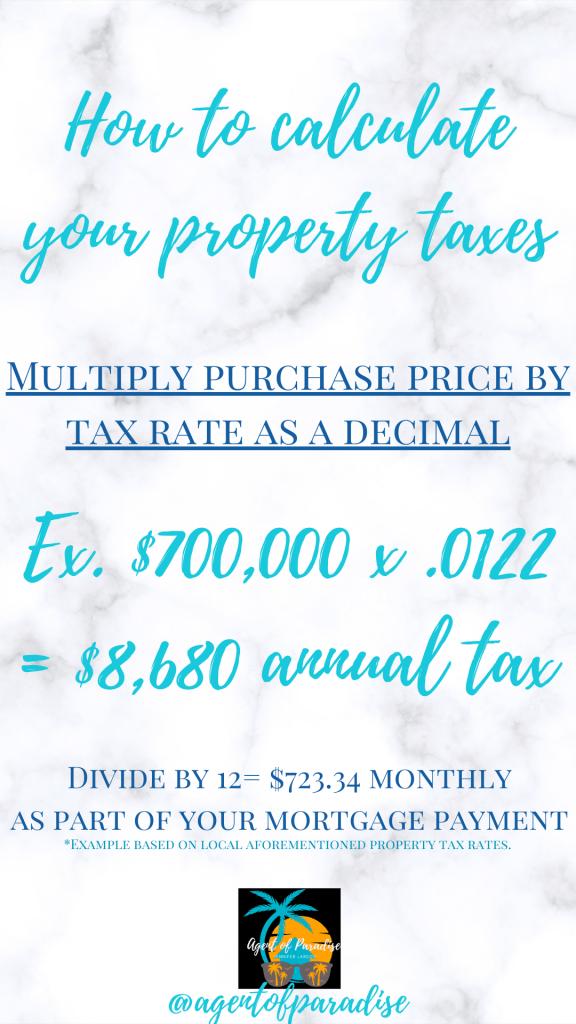

There are phone numbers listed for you to call if you have questions regarding your tax rate and tax bill. Here’s a quick snapshot how to calculate your taxes and estimated amounts when buying a house or confirming your amount due:

Your current mortgage statement takes 1/12 every month and sends you an annual escrow analysis as required by law.

Check your statement! And when buying a home make sure the current owner is up to date on their taxes!! Here’s a real life example I found while checking a property history:

This house was listed for almost $2 million and I knew the owners!

Always check the property before buying and run a preliminary title report with your agent before offering or ASAP afterwards. Sometimes the seller will also have HOA liens too and expect the buyer to help their financial woes at escrow! As a buyer I wouldn’t negotiate to help cover a seller’s back taxes but some have a lot of gulf and will absolutely try to insist the buyer cover part of the bill during negotiations because those liens have to be paid to the county and city before escrow and the county recorder’s office will allow the sale to happen and transfer the deed. The seller may also not disclose it before asking for the concessions and many agents may not even look it up before listing so they’re unaware at contract.

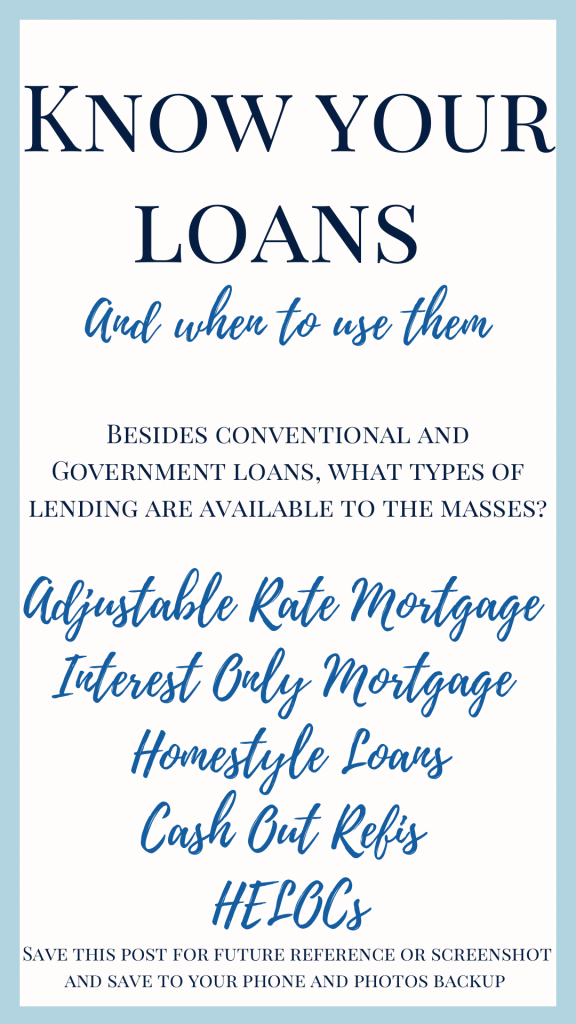

I’ll post a few information graphics below to share for you to research before applying.These are my last resort almost but good to know.

ARMs can get very expensive and these loans often are based on the PRIME Index (the Fed Rate) but even when the Fed lowers the rate a lot, you’re still paying a margin over the Fed Rate. The Prime Rate could be 4% but your ARM could still mean you’re paying 6-7% because of your margin on your loan. The Fed Rate is the base of the loan but rarely what you actually pay. You can get low rates in the beginning of ARMs and refinance as mortgage rates drop, if you qualify and have the money, but otherwise you’re stuck in them and they can rise to 10% easily at a lifetime cap. Be careful on these.

This is a VERY long term plan and best for experienced investors.These are one of the few FHA loans I prefer.

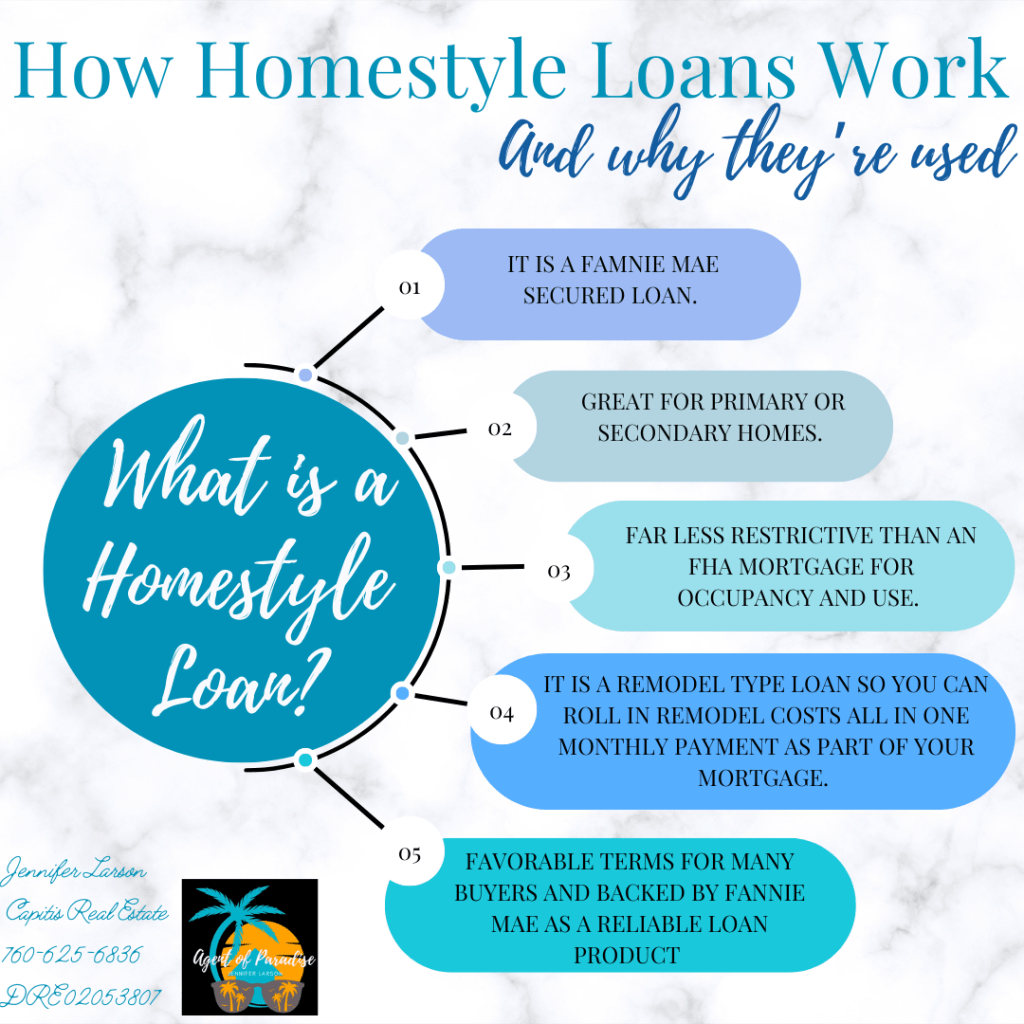

HomeStyle Loans are great because even though they are FHA they don’t have the rules and regulations of FHA. From day one you can use them for STR, flips, LTR, etc and they roll in the construction costs and they actually force the GC to be accountable. These loans require a 6 month turnaround, only approved contractors and engineers, they disperse the funds based on work completed, and they do lots of inspections. I like these for the average person even if they don’t want to invest. They’re fantastic and in less expensive markets, they’re going to cover a lot and help you find a home you actually want to live in, that might currently be scary to consider.

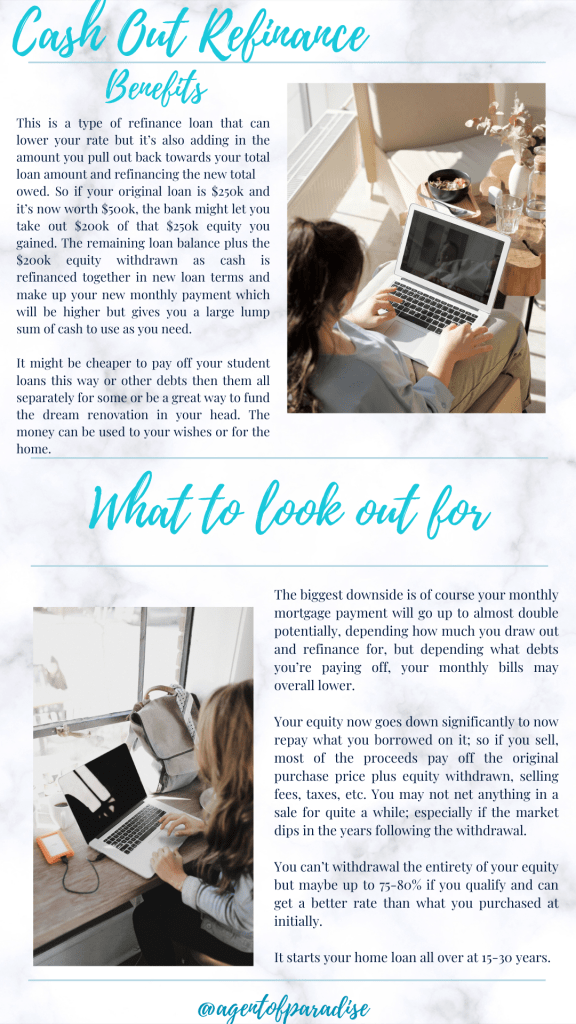

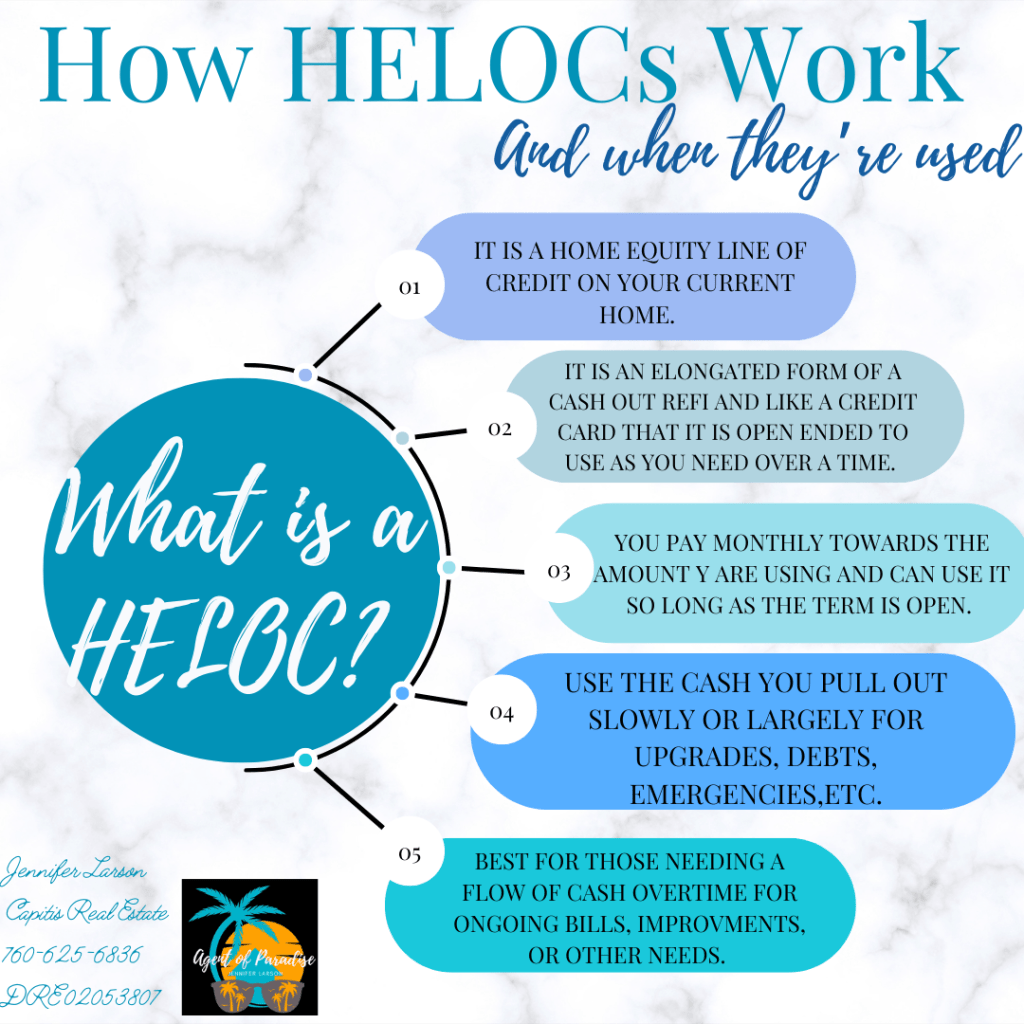

These are when you want cash but not to move.Understand these are a second mortgage against your house.

These can be great if used right and you’re smart with how you plan because it’s a loan against your home’s equity so understand you have to pay it back with your mortgage. Basically you refinance your house at its current value which is a lot higher and you after fees and taxes you get about 75% of your equity in cash to do as you please. This is where you need to be smart. Since you now have a bigger house payment don’t go buy more things. This should be used to pay off student loans, pay down all other debts, buy an investment property or pay one off, or you can use it to out kids through college etc, but be smart. It’s not free money and it can wreck you quick if you don’t get smart with it.

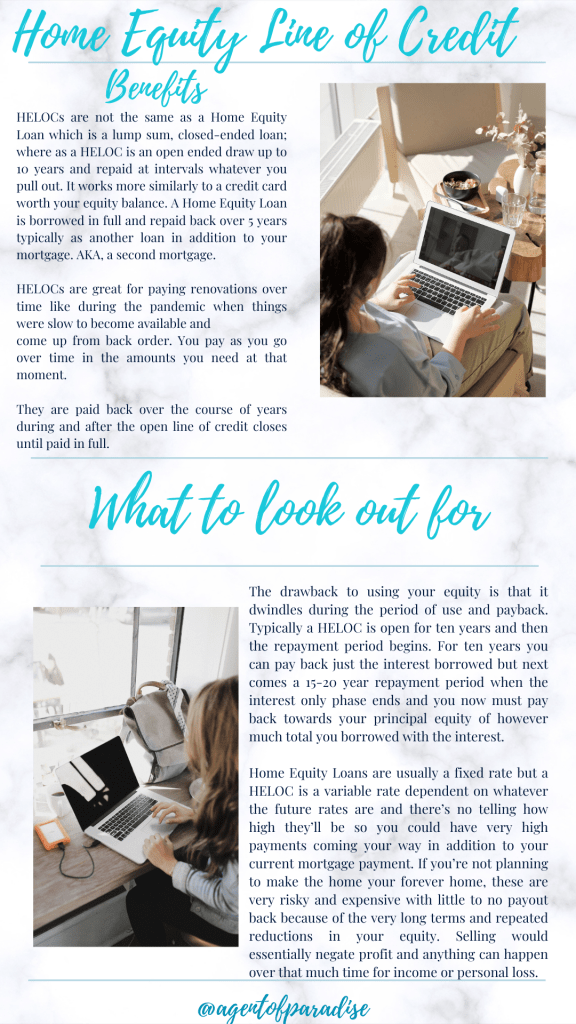

This is like an ongoing credit card against your house that expires.This is a line of credit you can use as much as you want as long as you keep paying down and it’s usually good for ten years. You can use it multiple times as long as you’re paying it down.

This is basically using your home’s equity as a credit card 💳. You can charge it up as much as you want and as long as you pay on it, for a decade you have this extra cash to use. However, like a credit can get you in trouble imagine how much trouble and debt you can incur with a six figure credit card limit if you’re being stupid with it. Again, this is best for life expenses like paying off all your other debts, student loans, renovations that put the equity back in, some do use it for weddings, paying off medical bills, using it to travel, etc. Have a PLAN with this and remember it’s a big credit card bill every month if you’re not using it wisely.

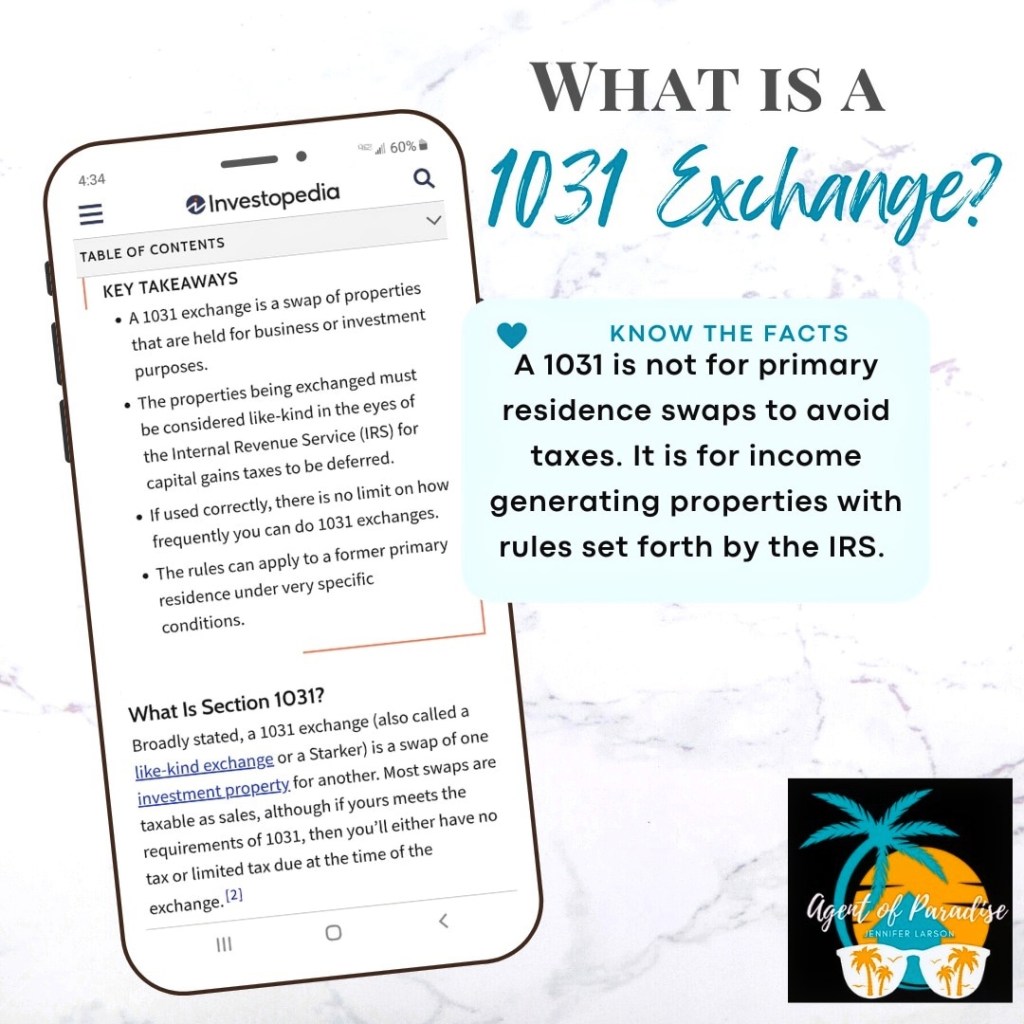

This is another option and you need a 1031 expert to facilitate the sale.

I have done these with clients and they work the same for us as agents on a 180 day deadline which is more than enough so long as you know what you’re buying, and get into contract relatively quickly. Escrows do get extended, canceled at the literal closing (been there) and other things can fall out and you have to start over again, maybe even with your home search and loan. I’ve had escrows that were supposed to close in two weeks suddenly take 4 months, multiple times. This kind of home purchase requires you to be smart with your time or you mess up your finances. You also need a 1031 Exchange agent because this is what’s called a Tax Deferred Sale and there is a lot of backend paperwork involved. It is a good option though!

Of course there are way more programs but these are the ones many people know but misunderstand the most in my experience. A good lender will show you all the options!!

Most people have this problem because money is hard to come by obviously. The answer to this age old question is throughout my blog and Instagram actually because it’s multi-faceted. You need the right savings and checking accounts like the MMA and HYSA and definitely a CD or two to keep that savings out of reach for spending but still earning great profits on your money. Those are all tools to grow your money.

To get more money I constantly share savings plans like $5 HYSA contributions or $100 per month, or swapping your streaming and television services for deposits into your account because that’s how money grows fast and gives your more time in life for the things that matter. I share a more efficient plan for those who can afford up to $250 per month and I share how to get to that and make the right cuts and changes to minimize the impact on your life but also maximize the impacts on your financial future.

How much do you need? Well, here’s a starting point to consider:

There’s a conventional first time buyer program that’s affordable at 3% down and no upfront MIP if you have good credit and income and haven’t been a homeowner for at least three years.

If you need a personalized savings plan, send a DM to @snowplowsanscacti and I can help you there.

If you need help, just DM me at @snowplowsandcacti on IG.

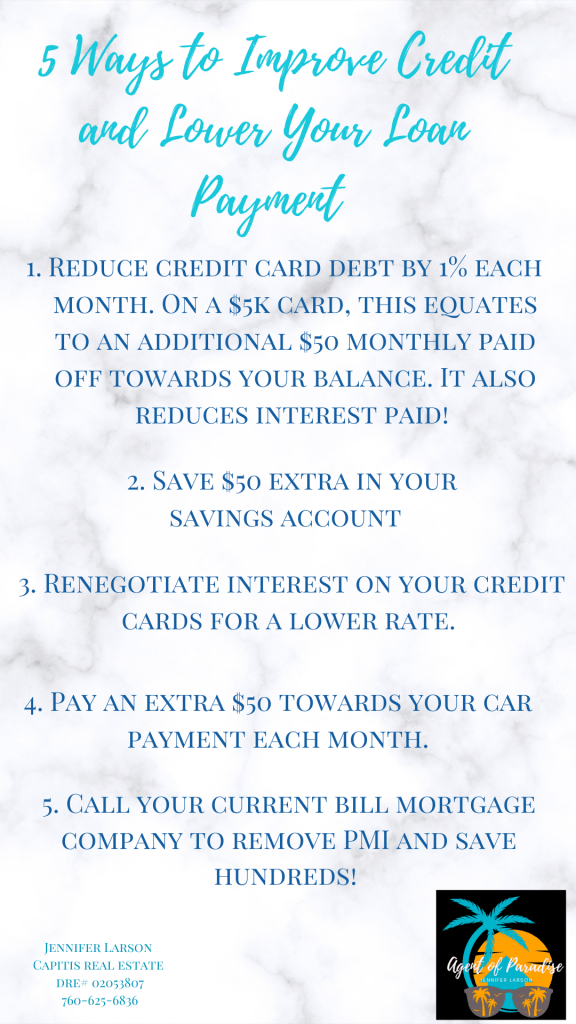

This is a good starting point if you’re thinking about buying a home one day. You have to be consistent with this. You don’t need to be debt free to get approved for a good rate usually, but you need a low debt load in order to get the best rate and lowest monthly payment possible.

Car loans are absolutely a killer to your approval chances, rates, and approval amount. The more debt you have, the more risk to the lender, so the more they’ll charge you to cover that risk. A lender is like an interviewer you want to look good and present yourself as best as you possibly can so make sure you have your finances in order and your credit cards aren’t charged high. Keep your balances, and usage low. It’s how much you CHARGE every month that matters and affects your score. Keep that in mind and don’t finance anything else in a monthly payment plan because that’s bad news for your loan application. Keep debt low and then you’ll have more to make your savings higher.

The more I look at rates, prices, the current affordability aspect of America, I do believe it’s time to revisit the aspect of doing a minimum 5%. You can do any amount technically that you want to put down, it’s just some programs have a minimum. If you have 7% down for what you’re seeing on Zillow, you can absolutely do that, and should if you’re financially ready. You can put any percentage down too if you decide it’s financially best for you to wait a few years and but say 12-15% down. What works best for your finances is when it’s best to buy. Yes, there are better markets than others and “buying the dip” certainly works well in real estate but it also needs to be when your finances are in a good place. Those factors need to coincide for it to be the right time to buy for you.

I know I sound like a broke record but I’m a huge believer in getting a high yield savings account and just putting money away. You don’t need a reason to save except to save. One day, your car is going to die. You might have an expensive medical issue in your family that’s going to pile on debt. You might want to have another child or begin a family. Maybe one day you’d like to go back to school if you can afford it and the kids are a little older. Maybe you’d like to buy a car in cash, even used, but you have no money. Even if you need tires one day, aren’t they so expensive and hard to afford because they go out at the worst times? Doesn’t it rent, then pour when you need sunshine the most? That’s why you need reserves.

So how do you build reserves on a very tight income? I always tell my clients to start with $25 per week or $50 per paycheck if you’re paid bi-weekly (every two weeks). Many people say they can’t even afford that, but, I know from experience, to do it. I have been there too. I spent many years not being able to afford the electricity and getting service shut off multiple times, only being able to pay part of the bill so I did to at least keep it on when I could. I was so sick of being broke and realized I needed to make a change. I figured if I’m already struggling to pay or can’t pay, I might as well struggle a tiny bit more but because I am putting money away. I walked or took the bus when I could to save on gas, or carpooling with coworkers. I got more frugal with not turning lights on, unplugging anything not in absolute need to be plugged in, stopped even turning the TV on, and opened the windows for a breeze instead of turning the fans on and learned to live with my AC not as cold as I wished. I saved A LOT or what was a lot to me at the time. I stopped with Netflix even way back then, lowered my interent plan, and cut the cable. All of those savings I added up. I think it was around $237 which was lifechanging at the same because I barely had $2.37 to my name, let alone without the decimal. I decided to put $200 of my paycheck contributions into my 401k in addition to the already $50 they autoenrolled per paycheck. They were matching our contributions at the time so I was getting the full amount. Years later when I left, I had a down payment for a house because I totally forgot about that account!! So did my husband. We built wealth from there with our condos, then houses. But to get started, it was those small amounts per paycheck changing everything and we didn’t even realize. It wasn’t a sacrifice it was the only reason we weren’t broke today.

Nowadays I know about tax implications of pulling out your 401k and filing that on your returns so now I know to just open an HYSA and put that money in. Don’t touch it! Let it rise like sourdough bread and see how it changes your life. Are on the same trajectory to be broke 5 years from now? Then get an HYSA and put money in it. You in 5 years will be a lot happier. Even if you don’t want to buy a house then or decide to wait another few years, you have a nest egg just to keep growing. One day you’ll have it for an emergency, a bigger downpayment so your mortgage will be smaller and easy to handle, or you won’t have to work until you’re 80. If you are hoping to buy a house one day, I would shoot for at least 5% down and remember that a starter home still works like a badass bank account to make you money in another 5 or so years, even better than an HYSA, and no asshole landlords to deal with! Don’t focus on buying your dream home but an improvement over what you have that you own and will grow your networth so when you sell, you get what you paid, and then a whole lot more. It’s better than renting for that reason alone but ONLY if it doesn’t stretch you too thin.