What is the URLA? The Uniform Residential Loan Application is the loan application you will fill out when applying for any type of mortgage. It is the basic paperwork of personal information needed to process the application, and financial details we need to determine your financial standing and run your credit. We need bank accounts, statements, employment documents, pay stubs, recurring bills, etc. If you have financial records for assets, additional properties like rentals are needed to determine eligibility and total gross income for all applicants on the loan. Different loans have different rules, and some loan programs are geared towards specific buyers, so the 1003 form will ask all these questions to help us find you the best loan product.

Screenshot of a page from the URLA

As you can see above, credit usage is part of the application and this will be critical in your approval. We will use this application as part of your pre-approval as well so you can put in offers for whatever house you are hoping to buy. During the approval process and underwriting, we will run your credit reports of course and continue to monitor your account balances and such; but we need to know for preapproval and get an initial idea of how we can process an application, and determine if you should right now.

Not only is it federal law to be accurate and truthful about your financial information, not disclosing all your balances and accounts will only harm you after your offer is accepted because when we begin digging into your bank accounts and check your credit history, this will become a major problem right away and you won’t get far into underwriting. You might get lucky and be able to pivot to another type of lending program but it can cause you to fall out of escrow and lose the house and a lot of money. Don’t hurt yourself and others by hiding what we are obligated and paid to find! It makes no sense but people do try it. Just be honest or wait to apply until you’re ready and comfortable with your money situation.

Real Estate agents love to talk themselves up on their social media channels to promote their business; but between all of the “success” stories and posts of new listings and sold homes, you need to look further into it. First of all, those can be posts of solds from long ago, their office listings versus personal listings, or one they worked on partially. They also don’t mean they are a great agent or the best for you. Top agents have failed many clients who needed more than just fancy video tours and advertising posts. Clients sometimes need agents who understand what they’re going through and why they’re moving. They need an agent that understands your perspective as a much younger buyer who has kids in the school system, how important location is to you, or other factors that too many agents gloss over because they think they know what is best for you. I’ve had to fire agents when home shopping for myself because a much older agent tried to tell me what I shouldn’t buy. Our first home budget was low so many agents wouldn’t even help us because we weren’t worth their time. Others would say “there’s nothing in that price range” when we found dozens on Zillow. They’d say “oh, those are condos.” Yeah, so? I would ask if they don’t show those and they’d tell us, “you don’t want a condo, it’s just a smaller place. Wait and get a house.” We finally found a nice agent but all he wanted to show us were homes he thought were best for us and only a couple from our list. When we found a few we really liked, yes, they were fixers, but we knew with our budget and our preapproval, we’d get something outdated and not exactly pretty compared to the rest of the market. We didn’t care. We just needed a place and were done dealing with horrible landlords. The last two we saw had great potential but he was trying to talk us out of them. We had already done the preapproval with him and the lender he introduced us to, but it was clear our time with him was over. We switched agents.

She was sometimes rough around the edges but she showed us what we asked for and gave some great points. We did have one disagreement that rubbed her the wrong way and she said we were wasting her time. We said fine and quickly scooted out the door. She took off frustrated and we figured, maybe we need to wait a few weeks and try again with yet another agent and a better understanding of what we want to help our next agent understand us better. An hour later, she called me and I reluctantly answered. She was the peppiest I’d heard her be. Well, she had calmed down quickly and checked out the last two properties on our list on her own and apparently, one convinced her we should buy it. “It’s perfect! It’s absolutely perfect. I’m still here. Come meet me and see it!” We were shocked but five minutes away so we drove right over and she was right! It was a cosmetic fixer but easy stuff and we did have some savings to paint and replace all the floors after close so we put in an offer at list price–it was priced to sell. We got it. It ended up a long and stressful escrow with issues on the seller side and we had to switch from an FHA loan to a conventional loan, as well as lenders when the original lender from our preapproval kept making mistakes. Finally, we closed. She stuck with us and everything was smooth through all of it. No agent is perfect and no agent relationship is hiccup free but she got the job done and was on the ball. Her communication was awesome and besides that one issue, nothing else was a problem. She was a great agent for us and did the best job of finding what didn’t exist according to some agents and she didn’t treat us like the low end buyers we were. We were newlyweds with a baby on the way but we were treated as if we were any other buyer. She worked for her pay and it took months instead of weeks, but she stuck with us and remained diligent. That’s a good agent. That home was our home for 8 years and it was a fixer that we spent those years slowly remodeling. We sold for a huge profit and bought us our next home without PMI. It was the right choice for us at the time and the other agent didn’t see that. We did because we know us and we weren’t as young and dumb as he assumed.

A bad agent can be a good person but telling a client what they want instead of showing them all options and letting them decide, is not what you should be hiring to help you. It’s YOUR money and your life. Make the decision, not them. Giving guidance is not the same as giving opinions so make sure you’re getting the advice you need versus unsolicited advice. When you hire an agent, make sure they’re listening to your needs, helping you make decisions but not making them for you, and ensure they’re focused on what YOU want to buy instead of what they want you to buy. You have to live in this place every minute of your life so make sure it’s for you and a choice by you. Make sure the lenders they refer you too are also very good.

Agents and lenders should be kind, understanding, great at listening and responding, communicative, timely, professional, and meet deadlines regularly. If they’re not picking up, timelines aren’t being met, unorganized, lazy, rude, or not acting in a way you expect, then don’t use them. Before you put in loan applications, do a prequalification first, before preapproval, and pay attention how they prioritize you, how they answer questions, how they provide information, how they provide documentation, how they correspond with you, and how they act. If you’re not sold on them, don’t waste your time. If you’re willing to proceed, then come back for preapproval but keep paying attention to them. Their prepparoval should be timely, the communication excellent, and answering all questions with knowledge and detail that helps you. The actual application begins when you get an accepted offer usually so proceed if you’re ready. If you ever feel you picked the wrong lender, tell your agent. If you feel your agent isn’t right, tell their broker in charge. Every state has different rules and times when you can switch agents so be sure you’re ready to get into escrow with your agent and lender before putting in offers. It’s crucial to have the right people BEFORE buying the house. Remember that offers are purchase contracts. They are legally binding documents and legal commitments stating the people involved, that they’re the ones getting paid at close, and that you are committed to using all those people in the contract as your real estate professionals. Buying a house is a legal procedure that can have consequences. You can be sued, fined, or worse if you try to violate the terms of the deal. It’s a real CONTRACT that must be honored and treated seriously. Make sure you trust who is on those forms with your signature.

The news makes the real estate market sound like a somber time but for buyers, this is THE time to buy a house. Why? Because when the market is this bad (one of the worst months in the last 30 years!) it means sellers are only selling because of a need right now. They might be relocating for work, financial reasons, divorce, other needs, and are having to sell in a difficult market knowing their home is going to sit for sale on average 3-4 months. It might even be creating a financail burden, as well as an additional stressor, so typically this creates a buyer’s market because these sellers need to sell soon. This means the market is ripe for buyers to have the upper hand and have all the leverage. Most sellers aren’t getting a lot of showings and open house guests nor offers so they’re stuck taking what they can get. Beggars can’t be choosers so if you’re interested in their home and you are the only offer they have received in weeks, you have the leverage to get yours accepted if it’s even remotely near their asking price. You also have the leverage to ask for seller credits to cover closing costs, or— rate buy downs. This is far more powerful than asking for $20k under list. A credit of the same amount, paid by the seller, nets them exactly the same BUT, it lowers your mortage payment far more than getting a discount on the total price.

Always remember: Your RATE is what makes your payment more expensive, not the sale price.

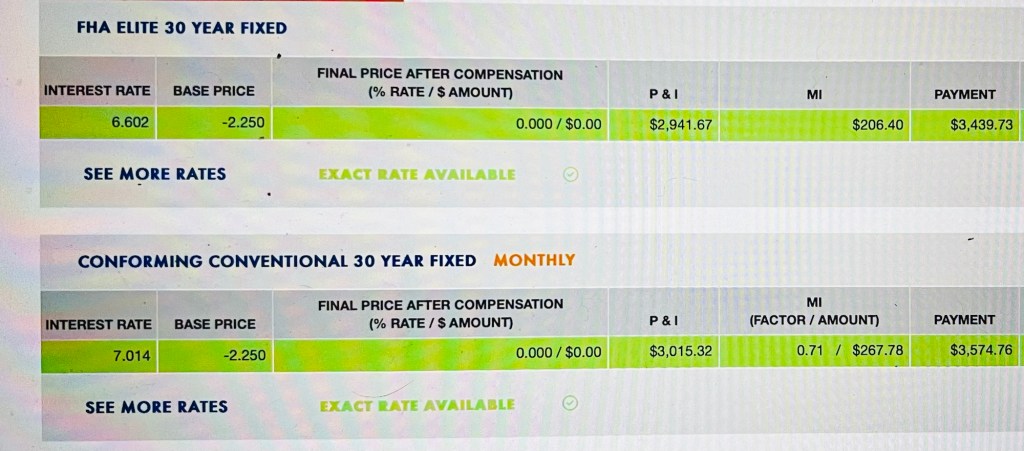

Allow me to demonstrate. Let’s say you purchase this house in Cathedral City, CA for twenty-five thousand under list price. Before taxes you and your spouse each gross about $4k every month or $48k per year before taxes. Your credit score averages to 715 and no other debts such as student loans, credit cards, or car payments. You have no HOA.

Listing from Capitis Real Estate

Your payment could look something like this with rates as of 10/8/2024:

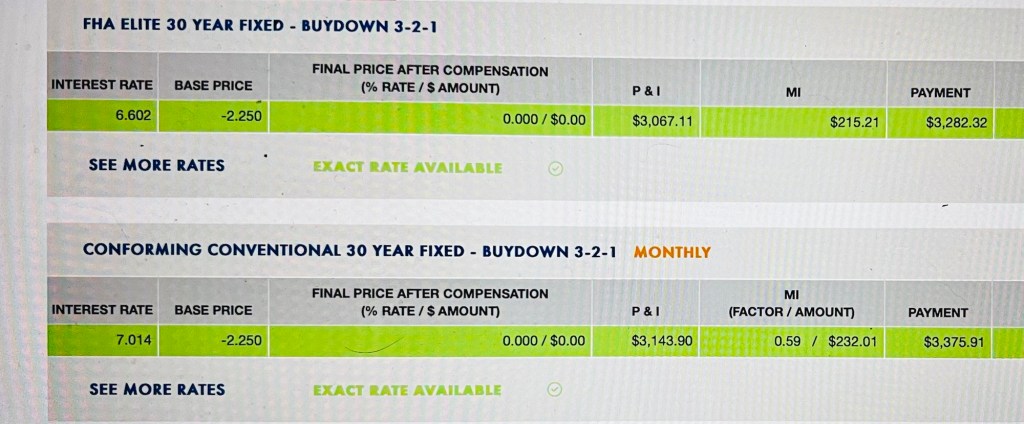

If you instead asked for the seller a credit to cover your rate buy down and get an approximate rate reduction based on a 3-2-1 buy down, here’s what you could pay every month while still paying list price and giving the seller essentially the same offer:

Mortgage estimates depending on credit, day, DTI, gross income, loan type, and other factors

See the difference? A good agent knows this and won’t suggest a price drop but instead a real way for you to save on your monthly payment. You do NOT need to wait for rates to drop to get a better APR, you just need the right agent and lender to get you there.

If you need a real estate agent who can help you negotiate the best deal and find you a home in your payment range anywhere in the country, email agentofparadise@gmail.com and I’ll send a you a referral depending on the area you need for buying and/or selling. If you need a lender in California, I can help with that too! Send me an email and we can set up a time to talk or get your application started. I look forward to helping you any way I can.

Rates are down and they continue to trend that way as inflation cools and home sales are slow in many areas. This is the best buyer’s market we’ve seen in a few years and it’s also a treasure trove of savings if you have the right strategy.

Even with rates in the low 6’s, buyers in slow markets have an advantage of getting motivated sellers to work with them. Instead of asking for $15k-20k off the sales price, a buyer will actually save HUNDREDS more per month on their monthly mortgage payment by, instead, asking for that amount in seller credits to buy down their rate in a 2-1 buydown. The buyers will then get a rate in the LOW 4’s for the first year and a 1% reduction the next year because of it. Buy down points are expensive and can easily cost thousands so if a buyer instead asks for the reduction as a credit versus a sales price drop, they’ll actually save significantly more. Just offering $20k below ask doesn’t save you much, believe it or not, on your loan. It’s all in the interest rate how much you pay and how you’re approved of what you can afford. Don’t worry so much about the price but how much you will pay per month. Here are some examples how it makes a big difference:

We’re going to compare this listing in Yucca Valley, CA from C & S Real Estate with a price reduction and a buy down scenario to show you the real way to save money on buying your next house.

Listing Agent Sean Dittmer and currently for sale as of this posting

If the buyer offers $20k below ask, their mortgage would be looking like this:

This is based upon an accepted offer $20k below asking and about 3.5% down or $13,000

If they instead asked for that in seller credits to buy down their rate, their payment would be approximately this: See the difference?

This is asking price but 2-1 buydown rate. Discount points are where it’s at! The down payment only goes up to $14k as well.

This is the same buyer with a 690 credit score and $60,000 annual income.

See how offering well below ask doesn’t lower your payment as much as a buydown? You can also buy permanent discount points for that amount from the seller and buy down to that permanent rate of 5% that’s shown in the example. These are real calculations from UWM that we use to price a loan. Instead of offering $20,000 below asking price, get that amount to buydown your rate and pay lower than market. If your credit is better than this buyer, you can possibly end up paying a rate in the 4’s!

It’s important to note that the rate you’re approved for will go up a little on your Closing Disclosure (the CD) because it includes the APR which is your rate plus all your points and fees financed into the loan. The APR is your total cost of the loan percentage. Mortgage insurance (PMI or MIP) are included in that Annual Percentage Rate so that’s the final cost you will pay as a rate on your loan. The APR is that mortgage 💸 insurance, any fees and points, + interest rate for your total loan percentage (APR).

To get a total APR under 5% you need better credit. If you’re working on your credit still, make sure you reach out and work with me. It’s free and easy. If you’re ready to buy, THIS is how you get the best rate. Get those buy down points so you save money and the seller will net the same price. Win Win!

For a home loan, it’s not medical debt. In fact, the Biden Administration is focusing on passing legislation through Congress that would eliminate it from being considered in your credit score for many types of financing and home loans. It also depends on what your credit report says (go to http://www.annualcreditreport.com) and a detailed report will show this if lenders can see it or not but it’s not typically a factor to worry about for approval. The biggest hindrance might be your student loans.

Make sure you’re getting as much loan forgiveness as you can and negotiating with your creditors to reduce fees and interest rates. This will help lower your payments and DTI which helps you get approved for more. If you don’t have student loans, your next biggest hurdle is probably your car.

Cars of all brands are absolutely ridiculous nowadays. We have clients paying almost a thousand dollars for Fords and Toyotas and I’m not talking their top of the line models with extra features. It’s insane right now so imagine for luxury cars how that can affect your approval! Add up your car payments and that amount will be how much less you’re approved for in underwriting because that’s all DTI and those numbers are subtracted from your total approval. We start with your front end DTI which is just how much the house will cost you per month to buy. Your back end DTI then starts reducing that amount because we have to factor in your cars, your credit cards, payment plans you’re on, etc. If it’s on http://www.annualcreditreport.com and you pay monthly on it, it’s probably going to reduce your approval amount. Car payments by far are the biggest killers of dreams and buying a house. Don’t buy brand new, and get them two years old at least, to save thousands on dealer mark ups and depreciation.

Next is credit cards 💳. People use these like free money and they’re NOT! Before you apply for a mortgage, make sure you are below 15% utilization and don’t be surprised you have to pay below 10% to get approved. Clients need to understand their current balances due are a major factor because it’s debt we have to account for. Pay it down tremendously before applying. It doesn’t matter if you always pay in full, pay before you apply!!

These are the top debts to pay down (or off if you can) so that your chance of a new house isn’t ruined by all these payments. You can have debt and buy a house but you can’t have a lot of debt. Lenders want to see fiscally responsible borrowers and big car payments and credit card balances are not a good candidate for rates around 7%. Sorry. 🤷♀️

We all know the complications of buying in a market with 7% average interest rates, inflation on gas and groceries, and home prices not coming down as much as expected. Millions of Americans feel they’ll never qualify for a home; or at least for the foreseeable future, because they can’t qualify at these rates and prices. If you feel this way too, maybe you need to open to other avenues to homeownership.

For example, you live in an expensive state like California, Florida, Texas, Idaho, Utah, etc, or an expensive city area elsewhere. Prices and rates near you might not be attainable because you don’t qualify based on income so you feel stuck and left out. For clients in this situation, I tell them there is hope but they need to be open-minded and creative with their solutions. I recommend a couple of things depending on what they can be approved for and their goals.

If you can afford something in your area but it’s not what you want, think about where you are and why you’re house hunting to begin with. Do you hate renting? Are you unhappy where you are? Are you being forced to move for any reason? Are you relocating and hoping to purchase? Do you want more for your kids or need more space? Understand your greatest pain points first and decide your top 3 non-negotiables. You will never get them all and probably not many more than that so make sacrifices to pick and choose your battles for the most important reasons you wanted to buy. Your reasons can be as simple and honest as wanting to build equity and wealth but it can also be you’re in a horrible situation or have the worst landlord and you want better for your future. The main reason for moving is the main factor in determining which creative strategy to consider and how to go about it.

For many though, I recommend looking within an hour of your desired neighborhood and just consider the next five years in a place you hadn’t wanted to even venture to. Does it mean living that far away? Not necessarily, but it’s an exploratory process to see what’s possible and what you might be willing to work with; or what might work FOR you. The difference is buying a residence to buy and hold for a couple of years or buying a property to use as some type of rental for 2-3 years while benefiting from the tax write-offs, the profits, and the equity building as time and maintenance keep it going. The other strategy is to be willing to sacrifice what you want for what can help you get what you want in 2-5 years. There are many cliches in life that people hate and it’s funny because they hate what’s true. For example:

Get comfortable being uncomfortable.

Most people aren’t comfortable getting a two-bedroom when they “need” a three. Most people won’t let their kids share a room these days, have a home office corner in their master, or work at the dining room table. Most people won’t accept not having a garage or a big yard. Most people won’t accept being uncomfortable for a short-term loss to experience the long-term gain; so what happens? Their current long-term becomes their long-haul or forever term because they weren’t willing to make sacrifices in life and weren’t willing to apply principles. Pride is not as prideful as people think. You rarely win with it and you rarely walk away with it.

To win in a market you otherwise wouldn’t be allowed to play in, you need to be willing to get in the game however you’re invited. The best way I find for most people who are willing to try, is to buy something not quite what they wanted but can make it work for them. I believe this is effective especially if they’re in an apartment currently, to build equity over time, get the tax benefits, and have a place to make their own better than they are as of now, allowed within their current rental. Maybe they buy a condo for a bit, a smaller home than they previously considered, or not get the amenities they greatly hoped for in exchange for the bigger picture of the near future. Can the home you settle for now help you settle into the home you wouldn’t otherwise be able to obtain in five years without the equity that would build in that time? Can you save or generate more income if you use it as a type of rental in the meantime?

For other hopeful buyers who are willing to do what it takes, I even suggest they buy out of area or out of state and start with a small rental property to build equity, make a profit every month, benefit from tax breaks, and save for themselves during this time so that in five years, their situation isn’t the same as it is where they stand today. It’s a fantastic plan for millions of people who don’t even know it, or want to believe it, but it also comes back to your goals and what I mentioned earlier–the pain points of why you wanted to buy and move in the first place. It matters when deciding if you can follow these ideas, however, your biggest hindrance why you CAN’T make it happen, might be the bigger reason why you should.

If those ideas are off the table regardless of the conversations we hold, then I can suggest my debt paydown and savings programs, free to anyone and everyone, and we go from there. The more you’re willing to think out of the box though, the more likely you are to get what you want in life.

If you’re interested in those debt and savings plans like my Road to 800 then email jenniferlarsonent@yahoo.com with “800” in the subject line.

You need all of your current financial documents and you must fill in a complete Uniform Residential Loan Application URLA 1003 form through your trusted lender. Almost every loan requires this application and an MLO cannot process anything without it first.

This is what I use to pull a customer’s credit and get all of their information for escrow. You need two years of pay stubs, a couple months of recent bank statements, and any other financial paperwork you’re going to use for your approval chances. If you have been divorced and pay alimony and child support, we need that. If you receive it, it is at your discretion to use it or not. You do not have to disclose unless you wish for it to be included in your monthly income. If your partner is applying too, I need their information and they must apply jointly with any of their current financial documents. You cannot use their income without also using their credit. If it’s a lot lower, that will hurt your chances because we use that lower number as our base.

On the application, you will fill in everything about you, your employers, your income, expenses, debts including current credit card balances, any property you already own, and what you’re applying for. If you don’t already have a home or budget in mind, we’ll skip that until you put in an offer. Just a note: There is some demographic information at the bottom of the application that we must legally fill in if a client refuses, per federal law, based on our assumptions and physical guess. This is required to verify discrimination and equality of loans in all areas, including underserved communities where diversity is low to ensure loans are being accurately processed and routinely funded in those areas. All buyers have equal rights regardless of any background and are to be approved solely on the merits of their financials and credit.

If you’re planning to buy this year, any money you will use as down payment needs to be in a legitimate account. Any “mattress money”, offshore accounts, piggy bank funds, gifts from family, etc. must be in a bank account at least 60 days prior. Any large deposits without a paper trail and proof of origin cannot be used. Put your money into an HYSA High Yield Savings Account, like SoFi, and let it grow on high interest there until you’re ready. In fact, all savings should be in one anyway.

If you don’t have a SoFi account, I have a free referral link for a sign up bonus that gets you extra money so email me at agentofparadise@gmail.com and I’ll send it to you.

Let’s calculate it for a variety of different home prices. Regardless of mortgage rates, this is how much you need to save for a down payment at 3% or 7% because they’re based on the math of the sale price, not the interest rates. How much you need to make though IS dependent on rates so that math changes.

Let’s start with a $200,000 house on an FHA 3.5% down. On your calculator type in 3.5 and hit % to get a decimal of 0.035 and then X 200,000=$7,000 and your closing costs will be at least that much for a total of $7,000 (more in some states) so in this scenario I’d advise clients to have at least $15,000 plus for inspections, and buyer agency compensation if necessary. I tell clients expect your total cash to close will be at least double your down payment in any state. In other states, it’s higher.

Let’s say you want the house but the roof needs to be repaird and the seller isn’t about to fully cover the full cost of something they’re never going to benefit from. (They say that all the time in negotiations!) You might have to meet in the middle with that expense if you really want the house and in seller’s markets, they have that leverage so multiple houses you look at might have this scenario. This is why so many buyers get blindsided by closing costs because all the money needed to bring the deal together can add up through the transaction. This is where it’s important to have additional savings or go back and negotiate seller concessions too. For the seller, they can be pay things at closing from the proceeds to compensate you some costs. You can have them cover what you covered on the roof out of pocket in seller credits, etc. No down payment loans are even higher interest rate and you’re approved for less so keep that in mind. You might not qualify for the house you want anymore. I have seen many times the “double your down payment” rule doesn’t work. I recommend more to avoid stress, surprises, and to know you’re in good standing.

All this to say, for each price, my rule of thumb (to also account for negotiations, inspections, and other fees you’ll pay during escrow) I tell clients, if you have 10% of the total purchase price, you should be fine.

$200k=$20k, $300k=$30k, $400k=$40k, $500k=$50k etc. If you’re worried about the “new” NAR rulings and you might have to pay commissions if you want an agent to help you, these amounts should help cover. If the seller is insisting on lots of costs for you to share, make sure you and your agent fully discuss it or get some kind of compensation back (like closing concessions as much as your loan allows) before you shell out. Sometimes you have to walk away. Ask your lender too because there are limits but FHA and Conventional loan holders Fannie Mae/Freddie Mac announced they will not count commissions against buyers so that’s good news!! There are still loan limits how much you can receive in credits so be wary of that and ask upfront with your lender.

One thing to note too, is that lenders like to see cash reserves in your account. This is why it’s so important to save and why I tell clients to expect a minimum of 10% needed because it’s not just the down you’re going to have to pay. Closings costs are just as high or worse, and some clients won’t get approved without reserves. Otherwise, you’ll need seller concessions and/or gift funds from loved ones to help the deal close. I’ve seen it too many times people weren’t aware of this. That emergency fund is what they’re looking for in addition to your total cash to close amounts. When in doubt, save more!